Barrier Reverse Convertibles: How they work

Barrier Reverse Convertibles (BRCs) are the classics among structured products. They belong to the yield optimization category and are characterized by a predetermined coupon and a certain safety buffer. BRCs are interesting due to their attractive coupons and in markets that are trending sideways.

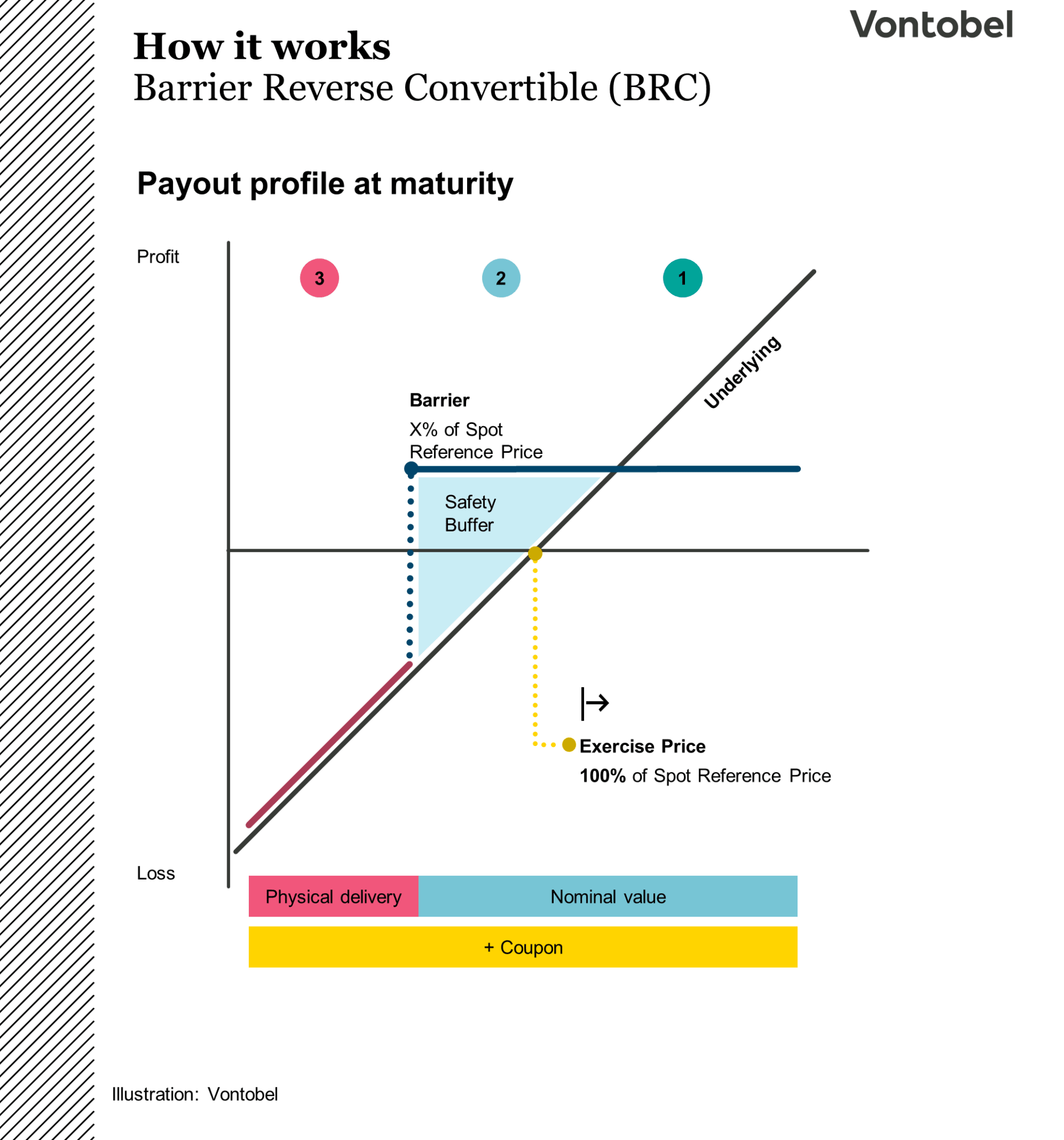

How a Barrier Reverse Convertible works

Barrier Reverse Convertibles (BRCs) are investment products that belong to the yield optimization category. BRCs are among the most popular structured products.

The key features of the product include the coupon and the barrier. BRCs also have a fixed maturity. The coupon is fixed in advance. Payment of the coupon is independent of the performance of the underlying asset. The barrier serves as a safety buffer. While the product is protected against price setbacks of the underlying up to the barrier, the potential return is limited to the coupon.

In principle, the lower the barrier (i.e. the protection against price setbacks of the underlying), the lower the coupon. The barrier is specified in relation to the price of the underlying at the time of initial fixing. During the term, it is observed whether the price of the underlying touches or falls below the barrier.

A barrier reverse convertible consists of at least one underlying, usually a share, but indices are also possible as underlyings. The price performance of the underlying is decisive for the repayment of the BRC at maturity. There are three possible redemption scenarios.

Scenarios

Scenario 1: The price of the underlying is at or above the strike price at maturity

In this scenario, it does not matter whether the barrier is touched or breached during the term. If the price of the underlying is at or above the strike price at the end of the term, the nominal value is repaid in full and the coupon is paid.

Scenario 2: The price of the underlying is below the strike price at maturity without touching the barrier

In this scenario, the price of the underlying is below the strike price at maturity, but the barrier has not been touched or undercut during the term. At maturity, the full nominal value is repaid plus the coupon payment.

Scenario 3: The price of the underlying asset has touched the barrier during the term and is below the strike price at maturity

In this scenario, the price of the underlying has touched or fallen below the barrier and the price of the underlying is below the strike price at maturity. The regular coupon payment and a physical delivery of the underlying or a cash settlement are made. The physical delivery or cash settlement is based on the specified number of underlyings (e.g. shares).

It should also be noted that investors bear the issuer risk in all scenarios.

Product variants

The classic BRC can be supplemented with different properties and additional features. The most important variants are mentioned below.

Single or Multi BRC

BRCs consist of at least one underlying. Multiple underlyings can also be used for one product. The product scenarios are similar, except that multiple underlyings are observed with regard to barrier and strike price. As the risk of touching or falling below the barrier is increased, the coupon is generally greater.

Click here for all classic barrier reverse convertibles

In the case of Multi BRCs, the type and amount of repayment is determined depending on the performance of the underlying with the worst price performance (which is why these products are often labeled “Worst-Of”). Even if all underlyings as a whole or individual underlyings perform positively, only the underlying with the worst performance is used to determine the repayment.

Click here for all classic Multi Barrier Reverse Convertibles

Barrier type: American or European

Barrier monitoring is generally carried out in two ways: continuously (American) or at maturity (European).

With the American barrier, the barrier is monitored continuously. This means that the price of an underlying asset is constantly monitored to see whether it touches or falls below the barrier. With the European barrier, it is only checked at maturity (at final fixing) whether an underlying touches or falls below the barrier. If the only difference between the two products is the type of barrier monitoring, the coupon will be higher for the product with American barrier monitoring.

Early repayment: Issuercallable and autocallable

Some BRCs offer the option of early redemption before maturity. In the event of early redemption, the nominal value is repaid in full together with a portion of the coupon depending on the term that has already elapsed.

In the case of an issuer-callable BRC, the issuer has the option of redeeming a product early on certain dates (observation dates).

In the case of an “autocallable” BRC, early redemption depends on the performance of the underlying securities. On the observation dates, the system checks whether the underlying is at or above a certain price level (call level). If this is the case, the product is redeemed early.

If there is no early redemption, the products are continued until the regular maturity date.

Products with the option of early redemption have higher coupons and / or lower barriers than products without the option of early redemption. With the option of early redemption, the exact maturity of the product is uncertain. The resulting reinvestment risk is rewarded with better product conditions.

Click here for all Callable Barrier Reverse Convertibles

Click here for all Multi Callable Barrier Reverse Convertibles

Advantages and Risks

Advantages

- Fixed, predetermined coupon payments

- Product takes effect when the underlying asset moves sideways

- Lower risk of loss than with a direct investment

- Safety buffer due to barrier

Risks

- Market risk of the underlying asset and risk of loss

- Limited earnings potential in the amount of the coupon

- No entitlement to dividend payments from the underlying

- Issuer risk