Outperformance Certificates: How they work

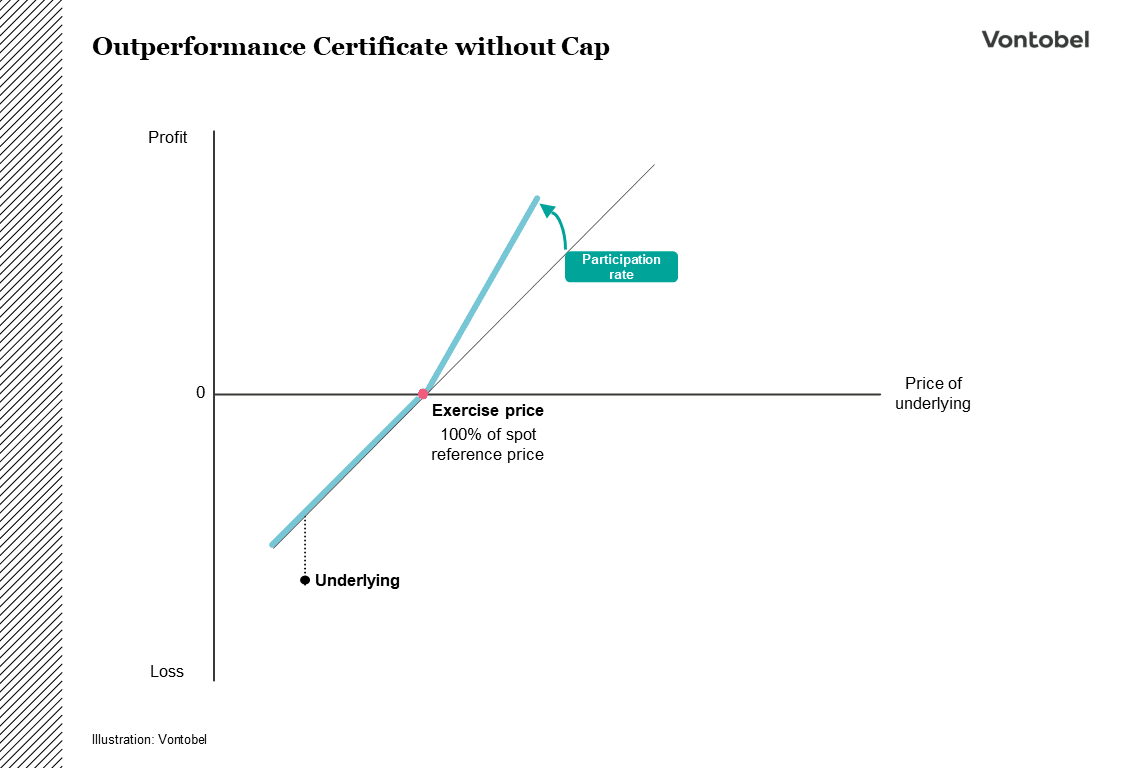

Outperformance Certificates offer investors the opportunity to participate disproportionately from rising prices of an underlying from a certain price level (exercise price) onwards. If the price of the underlying asset is at or above the exercise price at maturity, the investor participates in the price increase above the exercise price with a participation rate set at issuance (upper participation). Compared to a direct investment in the underlying asset, the investor can thus achieve a higher return. When prices fall below the exercise price, this participation factor does not apply. In this scenario, the investor bears the same risk as with a direct investment in the underlying asset.

Understanding Outperformance Certificates

Outperformance certificates fall under the category of investment products and offer investors who expect an underlying asset’s price to rise over a certain period an opportunity to optimize their return potential. This type of product allows for a disproportionate participation in price increases once a specific price level is reached. Typically, Outperformance Certificates are issued on individual stocks or stock indices.

An Outperformance certificate possesses three key features: the exercise price, the participation rate, and the term. The exercise price plays an important role as it determines at what level the participation comes into effect. The exact factor of this participation is determined by the participation rate set at issuance. Additionally, Outperformance Certificates always have a fixed term. If, at the end of the term, the price of the underlying asset is above the exercise price, the upper participation kicks in for the price increase beyond the exercise price.

The main features can be explained with the help of a small example. Let's assume an Outperformance Certificate on a stock with an exercise price of CHF 100, a participation rate of 2, and a ratio of 1. At the end of the term, the stock's price stands at CHF 110, which is above the exercise price. Since the certificate participates in the price increase of CHF 10 above the exercise price with a factor of 2, the investor receives CHF 120 at the end of the term (CHF 20 Participation & CHF 100 repayment of nominal value)

However, if the price of the underlying asset is below the exercise price at the end of the term, the participation rate does not apply. In the case of physical settlement, the investor receives the underlying asset in accordance with the ratio (number of underlying assets). Below the exercise price, the investor participates in a manner similar to a direct investment in the underlying asset and can potentially incur significant losses. In the context of the example mentioned above, a price of CHF 90 for the underlying asset at the end of the term would result in the physical delivery of one unit (ratio 1) of underlying stock (worth CHF 90), or an alternative cash settlement of the same amount. The representation below illustrates a comparison between an Outperformance Certificate and a direct investment.

How are Outperformance Certificates created?

An Outperformance Certificate consists of two option components. The first component is a Call option with a strike price near zero, also known as a LEPO (Low-Exercise-Price Option). This option grants the holder the right to buy the underlying asset at maturity for near zero. Therefore, the Call option has an intrinsic value equal to the price of the underlying asset and tracks its performance. In simpler terms, a LEPO behaves like a stock without the right to receive dividends.

Additionally, a Call option with a strike price corresponding to the current price of the underlying asset at the time of initial fixing, is required. If the price of the underlying is above the strike price at maturity, the option holder can acquire the underlying asset at a lower price than its current market value, resulting in a profit. In this scenario, a higher return can be provided compared to the value of the LEPO or the stock, depending on the participation rate. If the price of the underlying asset is below the strike price at the end of the term, the Call option expires worthless. Therefore, only the LEPO remains, allowing the delivery of the shares to the investor.

As the description above shows, options play a crucial role in structuring and pricing Outperformance Certificates. The price of an option depends not only on the price of the underlying asset during the term but also on factors such as the volatility of the underlying asset, time to maturity, and interest rates. These parameters influence the price of the Outperformance Certificate over its term. Therefore, investors should be aware that the participation rate may not necessarily apply at the specified level during the term. The payout profile depicted in the illustration above only applies at the end of the term, since the price of the underlying asset alone determines the repayment.

Variation: What is a Outperformance Certificate with Cap?

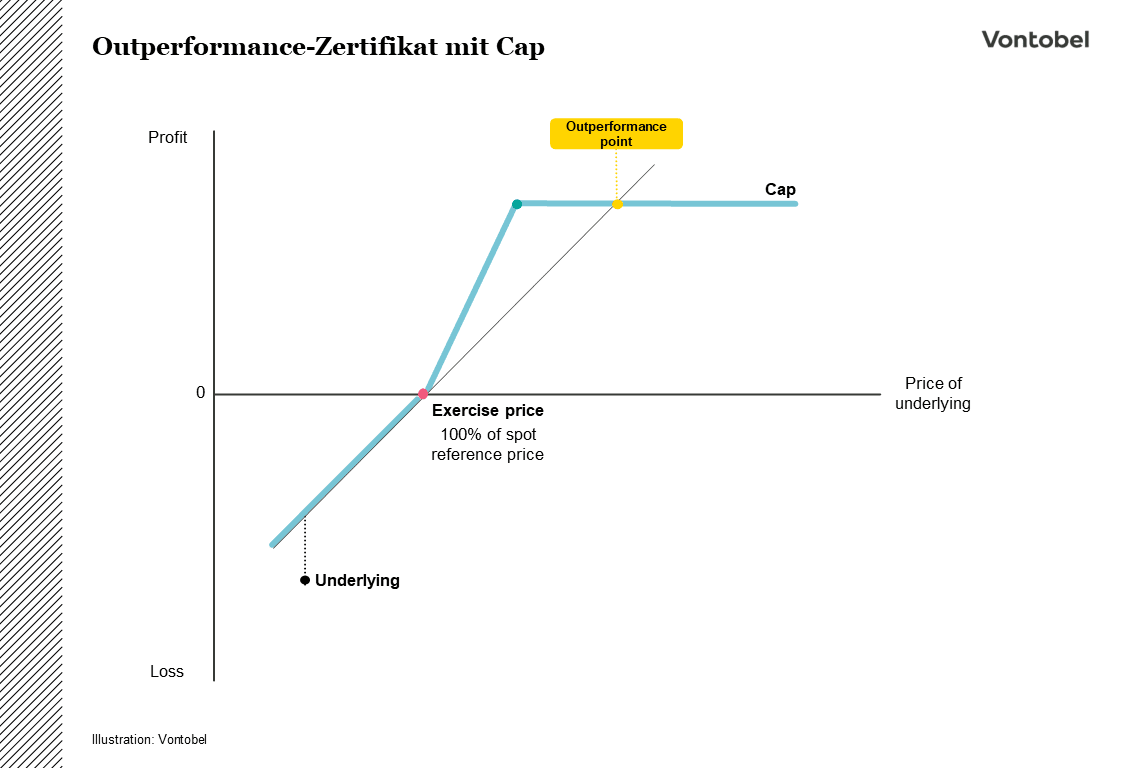

An Outperformance Certificate with Cap complements the traditional Outperformance Certificate by capping the maximum return. While it limits the profit potential for the investor, it can also result in a higher participation rate. This, in turn, can lead to significantly superior performance of the certificate within a certain range compared to a direct investment. Three features of the certificate are of particular importance in addition to the term: the exercise price, the cap, and the participation rate.

The exercise price, analogous to the regular Outperformance Certificate, is the price at which the disproportionate (upper) participation in the performance of the underlying asset begins. The cap is set above the exercise price and marks the point up to which the Outperformance certificate participates in the performance of the underlying asset. The cap, therefore, defines the maximum amount that can be realized in an optimal scenario. The participation rate, as before, indicates the extent to which the certificate participates in the positive performance of the underlying asset between the exercise price and the cap. It should be noted, however, that even with an Outperformance Certificate with Cap, the exact participation in the underlying asset's returns can only be realized at the end of the term. During the term, due to the product's structure, the participation rate may deviate from the stated value. Therefore, in addition to the mentioned features, investors should always pay attention to the product’s term.

Although no further gains are possible above the cap, the Outperformance Certificate with Cap, due to its disproportionate participation, surpasses even the direct investment beyond the cap. Nevertheless, in the case of strongly rising prices, an investment in the underlying asset is more profitable. The point at which this becomes the case is also referred to as the outperformance point.

Advantages and Risks of Outperformance Certificates

Advantages of Constant Leverage Certificates

-

Disproportionate participation in rising prices above the exercise price

-

No disproportionate losses below the exercise price

Risks of Constant Leverage Certificates

- Significant losses can occur in the case of falling prices, similar to a direct investment

- Pricing during the term depends on the options components

- Outperformance certificates with a Cap limit profit potential

- Issuer risk