Constant Leverage Certificates: How they work

Constant Leverage Certificates (CLCs) allow investors to participate in the performance of an underlying asset with leverage. They are equipped with a constant leverage (factor) that multiplies the daily percentage change of the underlying asset. With Long CLCs, investors can bet on rising prices, while Short CLCs allow them to bet on falling prices of the underlying assets. These products are suitable for short-term investment horizons and are not intended for a buy-and-hold strategy.

How Constant Leverage Certificates Work: Daily Performance with Constant Leverage

Proportional Participation

Short-term-oriented investors can use Constant Leverage Certificates to participate disproportionately in the daily performance of an underlying asset. Long Constant Leverage Certificates allow investors to bet on rising prices of an underlying asset, while Short Constant Leverage Certificates provide the opportunity to bet on falling prices. It is important to note that leverage works in both directions. This means that not only high profits but also equally high losses, up to the total loss of the invested capital, can occur.

The leverage effect of CLCs arises because investors require less capital compared to a direct investment. This means that the prices of Constant Leverage Certificates move more strongly than the underlying asset by the leverage factor.

The central element of this product category is the constant leverage. Unlike other products such as Warrants, Warrants with Knock-Out, or Mini Futures, where the leverage changes with the price movement of the product, the leverage (factor) of a Constant Leverage Certificate remains constant. The extent to which an investor participates in the performance of the underlying asset depends on the leverage (also known as leverage factor).

Leverage describes how strongly a product reacts to price changes in the underlying asset. This enables disproportionate participation. The higher the leverage, the greater the profit opportunities – but also the risk of losses. This is because leverage works in both directions.

Daily Performance

Let’s look at a small example: If an investor invests in a Long Constant Leverage Certificate with a leverage of 5, and the underlying asset rises by 1 percent within a single day (calculation day), the product value increases by approximately 5 percent. It is crucial to understand that the daily performance of the underlying asset is relevant. The performance of the product cannot be directly compared to the price development of the underlying asset over a longer time horizon. The reason lies in the path dependency that arises with Constant Leverage Certificates over an extended holding period.

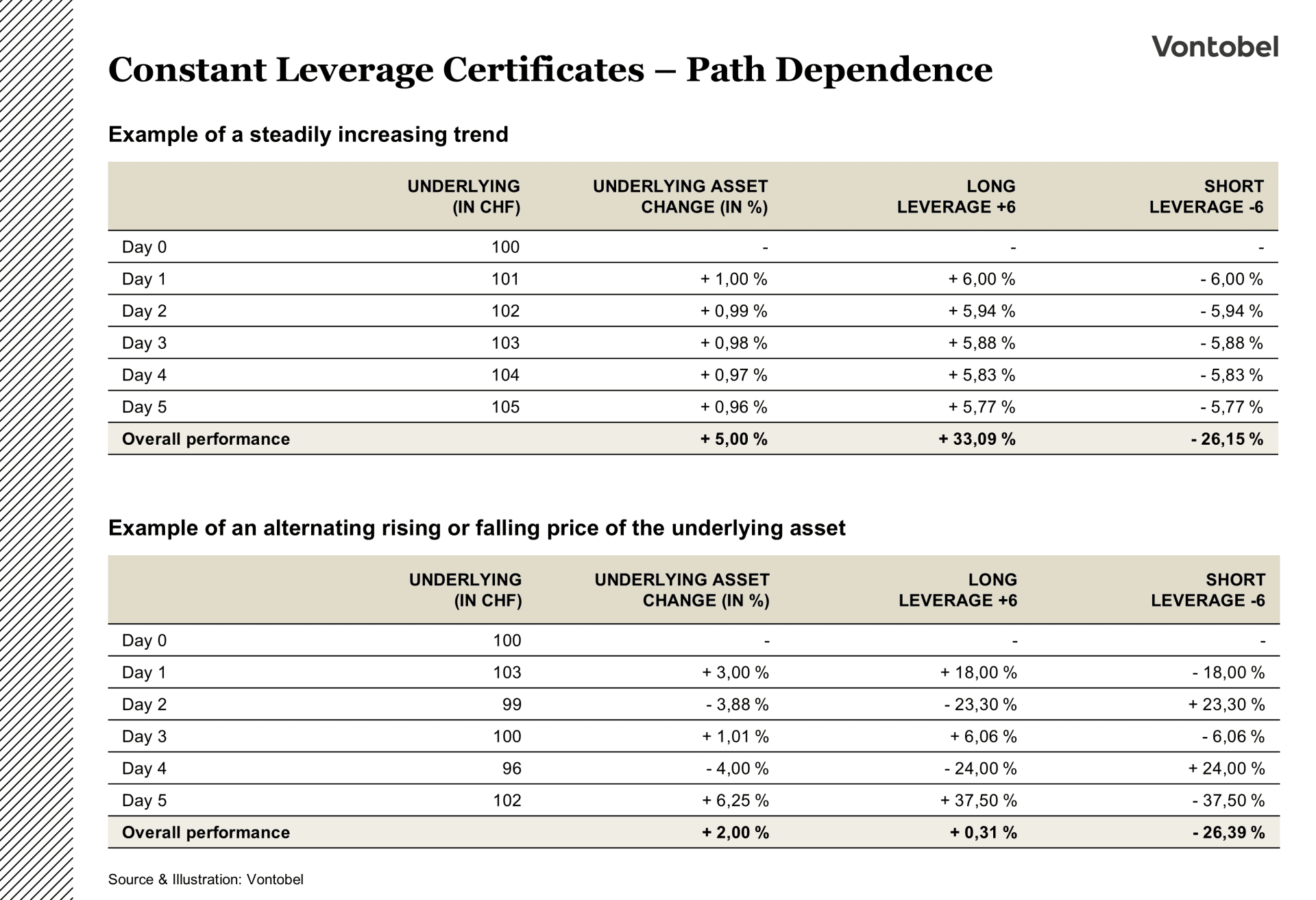

Path Dependency

A Constant Leverage Certificate leverages daily returns. Therefore, it is not possible to simply multiply the long-term performance of the underlying asset by a factor to determine the performance of the Constant Leverage Certificate. Instead, the daily performance must be calculated relative to the last valuation price. This chaining of daily returns leads to path dependency.

In other words, the performance of a Constant Leverage Certificate depends not only on the performance of the underlying asset but also on the specific sequence and timing of daily returns.

The significance of a clear, steady price trend or a sideways movement on the performance is illustrated in the following two examples. These examples also demonstrate the characteristic of path dependency.

Structure of a Constant Leverage Certificate

Constant Leverage Certificates directly replicate the daily performance of an underlying asset, simply multiplied by a factor. The performance is determined by the change in the underlying asset relative to the last valuation price.

In Constant Leverage Certificates, the daily performance of the underlying asset is reflected through the so-called capital value. This value is calculated at the end of each calculation day and shows the respective leveraged daily performance of the underlying asset. Simply put, the current capital value is adjusted at the end of a calculation day by adding (for Long products in the case of a price increase in the underlying asset) or subtracting (for Short products in the case of a price increase in the underlying asset).

Example:

The capital value of a 5x Long Constant Leverage Certificate on the SMI® is CHF 15.00 on Day 1. The SMI® rises by 2 percent within the calculation period (1 day). The capital value thus increases to CHF 16.50 at the end of the period (excluding financing costs or dividend payments). The formula for calculating the new capital value of a Long product is:

Capital Value T = Capital Value T-1 * (1 + Leverage Component – Financing Component)

Here, the leverage component reflects the daily performance (2 percent) of the underlying asset, multiplied by the respective factor (5). The financing component reduces the capital value by the factor-weighted financing costs of one day (for Short products, these are added).

This is a simplified example, as the calculation of the capital value also incorporates dividends, current interest rates, calculation fees, and financing spreads. The current capital value can be found in the product history on the product detail page at markets.vontobel.com.

What else to consider with CLCs

Volatility has no direct impact on pricing.

Constant Leverage Certificates (CLCs) are usually issued without a maturity date (i.e., open-end). However, it is also possible for them to have a fixed maturity date. Investors should pay close attention to the specific terms of the CLCs they choose!

It is important to note that leverage works in both directions, meaning that both disproportionate gains and corresponding losses, up to a total loss of the investment, can result.

Intraday Adjustments

A distinctive feature of a Constant Leverage Certificate (CLC) is the threshold. It indicates the level of performance of the underlying asset since the last valuation at which an intraday adjustment occurs.

The threshold is expressed as a percentage, and its absolute value is determined after each valuation. For long products, the threshold represents the maximum allowable negative change in the value of the underlying asset since the last valuation before an intraday adjustment takes place. For short products, the threshold represents the maximum allowable positive change in the value of the underlying asset since the last valuation before an intraday adjustment occurs.

When the threshold is reached, an intraday adjustment is triggered, and a new valuation price as well as a new (absolute) threshold are established. The absolute value of the threshold is recalculated after a regular daily valuation and after any potential intraday adjustment. The threshold exists to prevent an immediate total loss.

Wide Range of Asset Classes

Constant Leverage Certificates (CLCs) are available for a variety of underlying assets across different asset classes. The represented asset classes include equities, equity indices, commodities, precious metals, interest instruments, currency pairs, and volatility indices.

Advantages of a Constant Leverage Certificate

- Participation with a constant factor (leverage)

- Volatility does not affect pricing

- Typically open-end (with issuer's termination right); in some cases, also available with a fixed maturity

Risks of a Constant Leverage Certificate

- Market risk of the underlying asset

- Leverage works in both directions; disproportionate losses up to a total loss are possible

- Unsuitable for sideways markets or market phases without a consistent price trend (path dependency)

- Intraday adjustment during significant adverse movements of the underlying asset is comparable to an immediate realization of the loss. This makes potential recovery in the future more difficult

- Issuer's termination right: The issuer can terminate the product with a specific notice period, ending its term. This results in repayment of the current value at the specified date

- Currency risk if the currency of the underlying asset differs from the product currency

- Issuer risk (default of the issuer)