Dividend season is just around the corner

Spring, along with Easter, blossoming flowers and thawing snow, is also the season for dividend hunters. Swiss companies traditionally distribute dividends in March, April and May, allowing investors to participate in the company's success. For many shares, the dividend paid out is an important part of the total return in addition to the share price performance - and the amount can vary greatly depending on the company.

Anyone who holds shares usually hopes for price gains. However, more defensive investors in particular often focus on the regular distribution of dividends. Many Swiss equities can boast attractive and stable dividend yields. In the run-up to the dividend season, it has been observed in the past that the prices of high-dividend stocks rise slightly. The reason for this lies in the closing date set by many companies: only those who hold the share in their portfolio by this date at the latest are entitled to the dividend payout. This rule leads to some investors investing in high-dividend stocks, which can cause demand and therefore share prices to rise in the short term. However, it should be noted that past share price trends and events are not reliable indicators of future performance (cash.ch, 7 February 2025).

Dividends as a performance booster

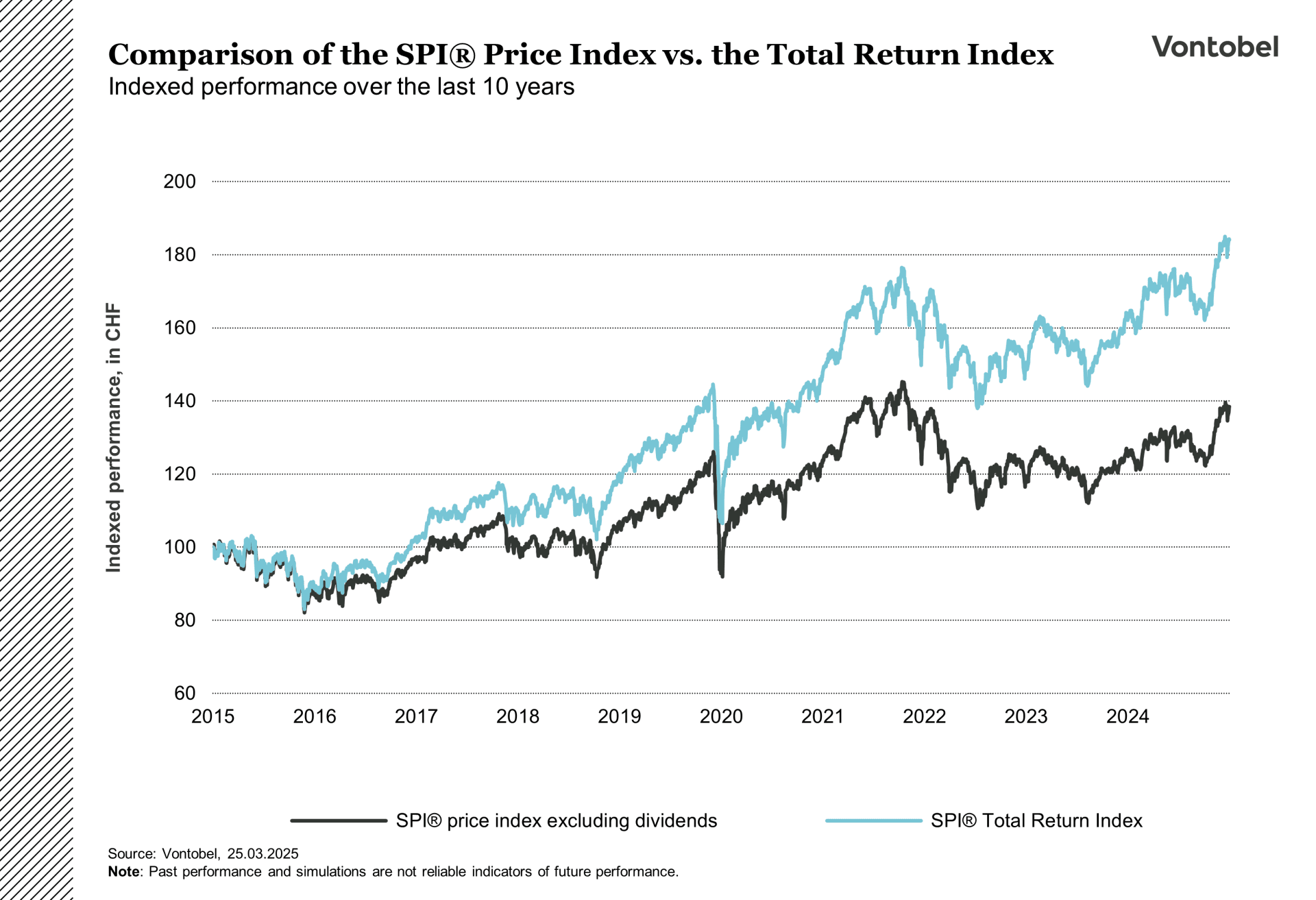

Dividends make a significant contribution to the overall performance of equity investments. The chart below compares the pure price performance of the shares included in the SPI® with the performance of the SPI®, which as a total return index also takes dividend payments into account. The SPI® comprises the share price performance of almost all Swiss companies listed on the stock exchange. Unlike the SMI® price index, which only tracks price performance, the SPI® shows the actual overall performance including dividends.

As can be seen from the chart, the dividends paid out make a significant contribution to the outperformance of the SPI® with dividends. This discrepancy shows how important dividends can be for overall performance, especially when looking at a longer period of time.

The average dividend yield of the SMI® is currently just under 3 per cent. This is slightly below the average for the past 9 years of around 3.26 per cent (Statista, 30. 01.2025). In an international comparison, the Swiss have nothing to hide: The dividend yield of the US equity market as measured by the S&P® 500 was 1.27 per cent as at the end of 2024 (YCharts, December 2024), while that of the EURO STOXX 50 is 2.56 per cent (Blackrock, 20.03.2025).

Dividend shares can flex their muscles, particularly in comparison with fixed-interest bonds. The SNB's interest rate cuts have led to a further increase in the difference between the dividend yield of Swiss companies compared to the Swiss risk-free interest rate (0.65 per cent on 20 March 2025).

The top dogs

The dividend policy of the ‘dividend aristocrats’ is once again taking centre stage this year. Companies that are labelled as dividend aristocrats have shown uninterrupted dividend increases for at least 10 years.

As in the previous year, the food giant Nestlé recorded a disappointing share price performance last year. The shares of the Vevey-based company lost just over 20 per cent. Nevertheless, Nestlé remained true to its position and increased its dividend for the past financial year by 5 centimes.

The telecommunications company Swisscom has long been a favourite, especially among more conservative investors, thanks to its high and constant dividend payouts combined with low share price fluctuations. After more than a decade of stagnating dividend payments at CHF 22, Swisscom has now announced an increase to CHF 26 for the 2025 financial year. Despite this positive development, however, there is some scepticism regarding the future development of dividends, particularly due to possible burdens from higher debt as a result of the takeover of Vodafone Italia.

In contrast, Zurich Insurance, for example, is more dynamic. The insurance group impresses with continuously rising dividends and was able to impress with a performance of around 23 per cent in 2024. Zurich announced a dividend increase of CHF 2 per share for the current financial year.

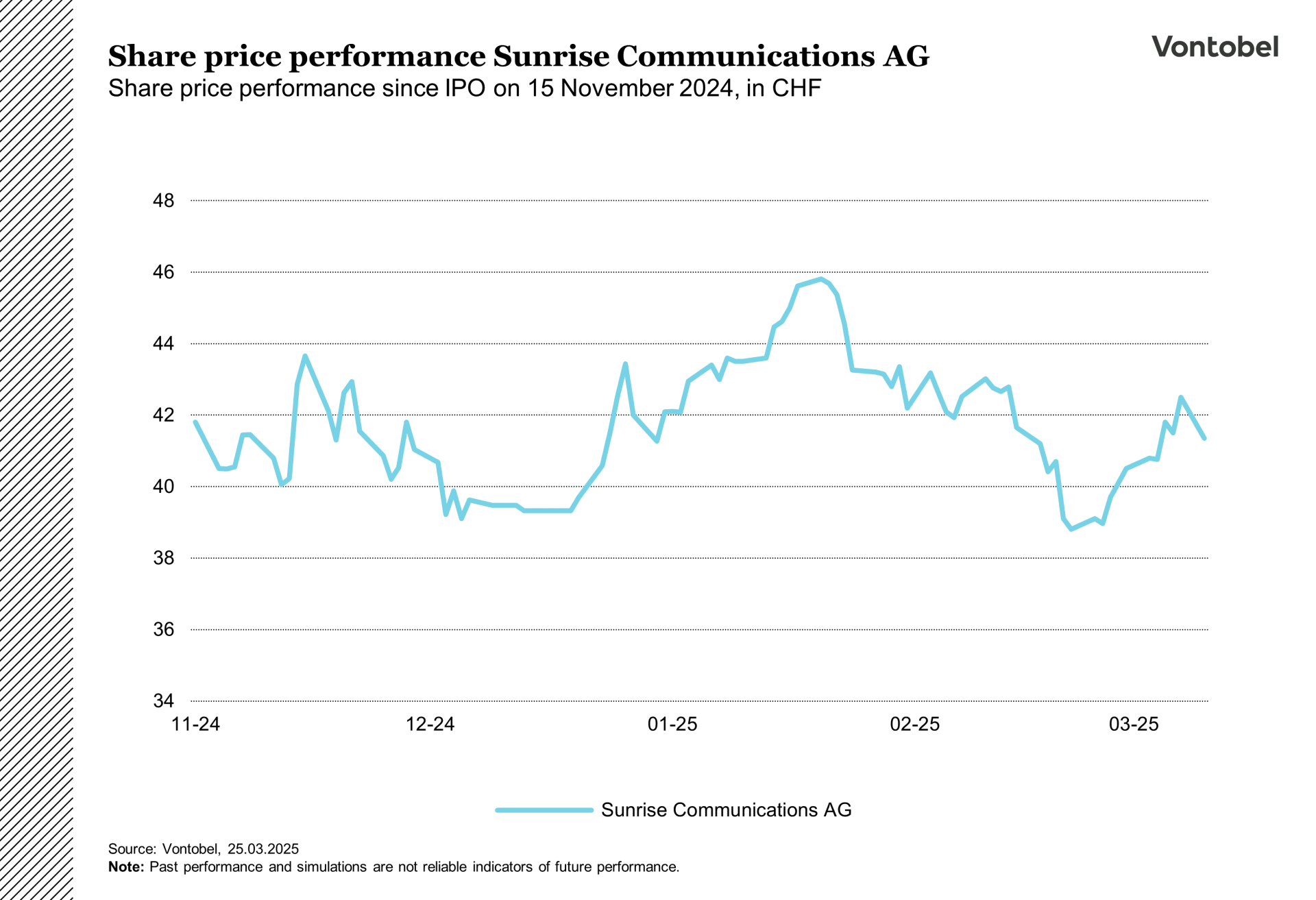

It is also worth taking a look at up-and-coming dividend stocks. One potential candidate is Sunrise, the telecoms provider that recently returned to the stock market. Although the share has barely got out of the starting blocks since its IPO at the end of 2024, the company offers one of the highest yields on the Swiss market at around 8 per cent.

The importance of dividends for structured products

Structured products enable investors to participate in the price performance of the underlying asset. If this underlying asset is a share, dividends can play an important role. In contrast to direct investments in shares, investors in structured products are not entitled to a dividend payment.

When structuring a structured product, the amount of the share dividend can have an influence on the individual parameters of the structured product. The reason for this lies in the individual components of a structured product. If we take a classic yield enhancement product such as the Barrier Reverse Convertible as an example, this product consists of two components: an option component and a bond component. Dividends are known to be one of the factors influencing the valuation and pricing of options and therefore have an impact on the option component of a structured product.

The higher the expected dividend yield of the underlying, the more attractive the characteristics of the structured product on the corresponding share could be. Changes in dividend expectations (e.g. an extraordinary dividend cut or cancellation of the dividend), for example as a result of a change in the business outlook, can have a direct or indirect impact on the valuation of structured products that have already been issued. It is therefore important to note that although dividends are not distributed directly to investors in structured products, they nevertheless play an important role in their design and for yield considerations.

In the case of participation products such as tracker certificates, which track the performance of the underlying asset almost one-to-one, dividends are handled differently depending on the type of product. In the case of certificates on price indices, which do not take into account the dividend distributions of the index members in the price performance, it is up to the issuer to decide whether it wishes to reinvest the dividends paid out. When purchasing such products, it is important for investors to find out about the issuer's approach to dividend payments.

To summarise, dividends can play an important role in the design and valuation of structured products. Investors should therefore consider the dividend policy of the underlying asset when investing in structured products.