Investors' Outlook: US tariffs - The dance is on

Markets two-step around risks Investors had plenty to juggle last month—improving economic growth, persistent inflation, and geopolitical tensions. The Multi Asset team maintains its outlook of steady growth, moderate inflation, and further central bank easing, which it believes would favor equities over bonds.

Trade war fears surged as headline after headline focused on levies on Chinese goods, or tariffs on all steel and aluminum imports as well as on cars, pharmaceuticals, and semiconductor chips. This hit US consumer sentiment and raised inflation concerns. However, if the first US-Chinese trade war is any guide, tariffs alone are unlikely to drive a sustained rise in goods prices. Instead, greater inflation risks could stem from mass repellings tightening the labor supply and pushing up wages or a tougher US stance on Iran—though an aggressive approach against Iran is rather unlikely. And while January’s US inflation came in hotter than expected, it’s unlikely to be a lasting trend. Early-year inflation spikes are common, as companies often adjust pricing at the start of the year.

Against this backdrop, there seems to be room for some interest-rate cuts this year. Markets are cautiously pricing in only 36 basis points (bps) of Fed cuts in 2025. The Fed’s March meeting will update its forecast (previously 50 bps). The European Central Bank and the Swiss National Bank may accelerate easing given Europe’s weak economy.

“Tariffs are the most beautiful word in the dictionary!”—Donald Trump

Trade protectionism has a long tradition in the US. But does it work? As the US again ramps up tariffs and trade restrictions, it’s worth taking a closer look at the history, impact, and potential future of protectionist policies.

Tariffs have always been a popular tool in US economic policy. The Tariff Act of 1816 introduced a 25 percent tax on wool and cotton goods imported from abroad, helping to create a budget surplus and fuel the country’s industrialization. By 1861, the Morrill Act entrenched a prolonged phase of protectionism—often championed by Republican presidents—which lasted until the passage of the Under wood-Simmons Tariff Act. The turning point came after World War II with the introduction of the General Agreement on Tariffs and Trade (GATT) in 1948, a landmark accord that paved the way for the World Trade Organization (WTO) in 1995. The WTO’s guiding principles remain the same today: reducing trade barriers, opening markets, and improving the integration of developing countries into the global economy.

Yet, while free trade is generally seen as beneficial in the long run, it has also brought unintended negative side effects. One glaring issue is the US trade deficit, which has ballooned to USD 118.7 billion—meaning the US imports significantly more than it exports. Trade deficits can negatively impact the domestic economy, weighing on productivity, employment, and even interest rates.

Already in the late 20th century—when the world was still caught up in free trade euphoria—a Donald Trump was already voicing his frustration over the flaws in global trade. In a 1987 interview with talk show host Larry King, he lamented: “A lot of people are tired of watching the other countries ripping off the United States. This is a great country.” By mid-2016, Trump’s rhetoric had sharpened. During a campaign speech at a metal recycling company, he accused Hillary Clinton of waging a “trade war” against American workers, alleging that she had backed “terrible deals (...) from NAFTA to China to South Korea.” He vowed that, under his leadership, the US would end this war and negotiate a “fair deal” for the American people.

What followed is now history (see chart 1). In January 2018, the Trump administration introduced a series of tariffs and trade barriers. While China, the world’s second-largest economy, was the primary target, other countries also found themselves in the crosshairs. The conflict quickly escalated. Within months, the US imposed a 25 percent tariff on Chinese imports, triggering swift retaliation from Beijing. By January 2020, after two years of economic brinkmanship, both sides brokered a Phase One Agreement, a fragile truce in which China pledged to increase US imports by USD 200 billion over two years.

2025: The return of the trade war

“Trade War 2.0” is taking shape. Once again, the focus is on countries running a trade surplus with the US (see chart 2). The latest round of tariffs encompasses 25 percent duties on imports from Mexico and Canada, 25 percent tariffs on aluminum and steel, and 20 percent tariffs on all Chinese goods. Additionally, Trump has proposed 25 percent tariffs on cars, pharmaceuticals, and semiconductor chips.

So, why does Trump love tariffs? Many US presidents have used tariffs, but Trump takes it a step further, famously calling them “the most beautiful word in the dictionary”. The Multi Asset team sees three key reasons: First, Trump views tariffs as a source of government income that can help reduce the US fiscal deficit and finance his campaign promises. His role model in this regard is William McKinley, a “great president” who, according to Trump, “made the US very rich.” Trump’s admiration for McKinley was so strong that he has issued an executive order to rename Denali, North America’s tallest mountain, back to “Mount McKinley.” Second, Trump sees tariffs as a shield for key national industries—whether by safeguarding US technological leadership in semiconductors or bringing back manufacturing jobs through “re-shoring” instead of “off-shoring.” Third, Trump considers tariffs a bargaining tool to advance broader policy goals, such as fighting the fentanyl crisis or pressuring NATO allies to increase military spending.

Downside risks for the economy, limited upside risks for inflation In the event of a full-blown Trade War 2.0, investors would likely be more concerned about the global and US economy than about inflation. Why? Simply put, tariffs disrupt nearly every economic player—they create uncertainty for both businesses and consumers alike. If taken too far, companies may scale back investments and hiring, while consumers respond by cutting back on spending. This domino effect weakens corporate earnings, consumer demand, and overall economic growth, potentially pushing the economy into a downturn. In such a scenario, any inflation concerns would largely resolve themselves as weaker demand cools price pressures.

A look at chart 3 shows that even Trade War 1.0 had only a limited impact on US goods inflation. One exception was tariffs on washing machines and parts, which in some cases soared to 50 percent, but even those prices started to fall again by the end of 2018. Perhaps new US Treasury Secretary Scott Bessent has a point when he argues that “tariffs can’t really be inflationary—because if the price of one thing rises, people have less money to spend on other things”…?

Conclusion: Trade wars probably don’t work

In the short term, tariffs can create market volatility, but in the long run, they fail to deliver lasting economic benefits. The increased US imports that China pledged under the Phase One Agreement have yet to be fully realized. While Covid-19 and its impact on global trade played a role, they don’t tell the whole story.

Nations affected by tariffs often find ways to adapt, limiting the intended economic pressure. One method is to diversify export routes. For example, China’s exports to developed markets have steadily declined, from nearly 60 percent before the trade war to about 50 percent by late 2024, while exports to other countries have surged (see chart 4). Trade has boomed particularly in countries like Vietnam (due to its proximity to China) and Mexico (due to its proximity to the US). Vietnam’s trade surplus with the US reached a record high of over USD 123 billion last year—a nearly 20 percent increase.

Another common strategy is currency devaluation, which can help offset higher tariffs. This was evident during Trade War 1.0, when China allowed the yuan to weaken beyond 7 per US dollar, its lowest level since the 2008 financial crisis. While President Xi Jinping has repeatedly emphasized the need for a “stable” currency, a renewed devaluation remains a real possibility if trade tensions escalate.

Chart 5 highlights another key issue: the effort to re-shore jobs has largely fallen short. One of the biggest hurdles is the stark wage gap between the US and other countries. According to the Bureau of Labor Statistics, by mid-2024, a US manufacturing worker earned nearly USD 30 per hour, compared to about USD 7 per hour in China—and even less in some other countries. This disparity, along with stricter safety and environmental regulations, raises production costs for US companies and shrinks profit margins.

Even mathematically, Trump will struggle to replicate McKinley’s “tariff king” legacy. McKinley governed at a time when federal spending was below 5 percent of gross domestic product (GDP). By 2023, that figure had surged past 22 percent, with the Congressional Budget Office projecting even further increases in the years ahead. In short, tariffs alone are nowhere near sufficient to fund today’s US government.

According to a poll by public policy research organization The CATO Institute, 55 percent of Americans have a favorable view of international trade, and 53 percent support free trade, while only 34 percent view tariffs positively. Trump’s “maximum pressure” trade policy is likely less about tariffs themselves and more about leveraging trade negotiations to secure good deals on the issues that truly matter to voters, namely inflation, health care, and the economy.(CATO Institute, 2024).

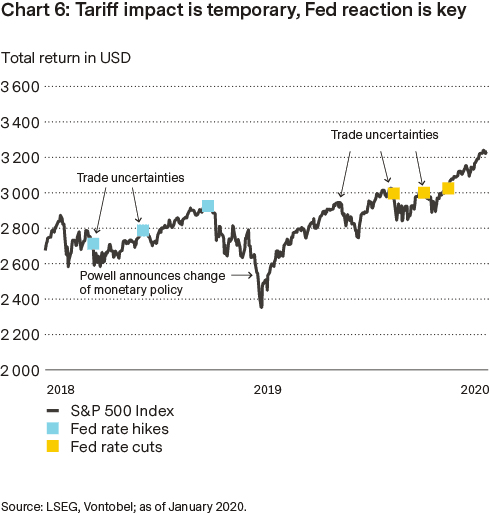

The Fed’s reaction is key

From an investor’s perspective, one key question is whether the Fed has learned from the last trade war. The Fed had already begun a tightening cycle in late 2016, continuing to raise interest rates throughout 2017 and 2018—essentially hiking straight into the trade war. By summer 2019, however, mounting pressure from nervous stock markets and growing concerns over slowing economic growth (see chart 6) forced the Fed to reverse course and cut rates. This time around, it’s crucial that the Fed recognizes temporary price spikes for what they are and avoids responding with even tighter monetary policy.

The Fed’s slow dance

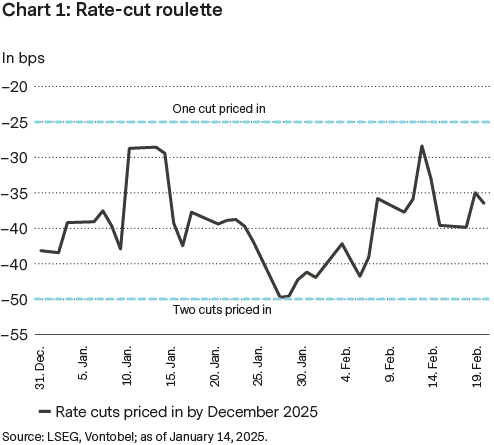

January’s Consumer Price Index report indicates that inflationary pressures remain, driving two-year and 10-year breakevens to multi-year highs. While the five-year, five-year gauge remains steady, short-term expectations have unsettled investors. Meanwhile, the Fed maintains a cautious stance, demanding clear evidence of disinflation before cutting rates. Markets are pricing in 1.6 cuts, around 40 bps for 2025, while the Fed’s guidance suggests a larger 63-bps move.

Despite markets reacting sharply, January’s inflation figures merely reinforced an inflationary trend long signaled by the data. The biggest market moves came in inflation breakevens, which reflect market-implied inflation expectations by comparing yields on nominal and inflation-linked government bonds. Rising breakevens signal that investors anticipate higher inflation over a bond’s maturity.

Shorter-dated breakevens hit two-year highs, while longer-dated measures also reached multi-year peaks. Meanwhile, the five-year, five-year forward gauge held steady, but rising short-term expectations highlight growing market anxiety over inflation risks. For the Fed, the data reinforces a patient stance, with any rate cut hinging on clear, sustained progress toward its inflation target. As Chair Jerome Powell recently noted, the Fed doesn’t overreact to a few months of strong or weak data—nor should markets.

Market expectations for Fed rate cuts this year have fluctuated between one and two cuts (see chart 1), with 1.6 cuts (40 bps) currently priced in. Nearly two months into the year, seven Federal Open Market Committee meetings remain, with a March pause highly likely, May all but certain, and June still a toss-up – leaving four “live” meetings for potential action. While markets expect 40 bps of easing, the Fed’s year-end median dot suggests a 63-bps reduction could be on the table.

Despite a flurry of executive orders, appointments, and policy moves, credit spreads remain remarkably stable, supported by persistent yield-driven demand and robust fundamentals. Credit spreads remain exceptionally tight (see chart 2), limiting room for further compression and heightening susceptibility to negative market developments or economic shocks. With less of a cushion, investors may find themselves more exposed to risk.

“Objects in mirror are closer than they appear”

The familiar safety warning engraved on passenger-side mirrors— “Objects in mirror are closer than they appear”—is a fitting analogy for China’s latest breakthrough in artificial intelligence (AI). DeepSeek’s game-changing development in January served as a wake-up call, proving that despite setbacks, China remains a formidable competitor in the global AI race.

The first months of 2025 have been shaped by major geopolitical and economic events, largely driven by US policies. From Russia-Ukraine peace talks that sidelined European allies to the looming threat of global tariffs and Washington’s mediation efforts in the Middle East, the US has been setting the global agenda.

But China has not been standing still. The People’s Bank of China is keeping liquidity flowing, cutting interest rates, and fueling credit growth to support markets. Meanwhile, Beijing is backing away from its crackdown phase on tech and property, focusing instead on measures to revive key industries. Direct stock market interventions have also intensified, sending a clear signal that stabilizing investor sentiment is now a priority. The Multi Asset team expects even more government stimulus in the coming months, boosting consumption and investment. All of the above could signal that after years of economic struggles, a turning point may finally be on the horizon.

Amid this backdrop, the Multi Asset team sees structural opportunities across key sectors in a market that’s still trading at a significant discount compared to developed economies (see chart 1). Companies like Huawei and DeepSeek are making strides in semiconductors and AI, strengthening China’s role as a serious global competitor. In green energy, China remains the dominant force in electric vehicles (EVs), solar panels, and battery production, riding the wave of the global energy transition. Despite ongoing geopolitical tensions, China remains a dominant export powerhouse—a global manufacturing hub with strong demand for high-tech and industrial goods. This could signal that Chinese manufacturers could easily absorb tariffs.

There also seems to be potential for a foreign investment revival, as global funds reassess Chinese assets—especially with US interest rates stabilizing and China’s stimulus kicking into gear. After years of negative sentiment (see chart 2), much of the pessimism is likely already priced in, meaning any positive policy shift or fundamental improvement could trigger a powerful rebound.

Coffee—the new “black gold”?

According to American author and environmentalist Edward Paul Abbey, “our culture runs on coffee and gasoline”, with “the first often tasting like the second”. While crude oil, the foundation of gasoline, has been trading in a comfortable range of USD 70 to 75 per barrel for months, the price of the coffee beans has been on a relentless upward trajectory.

Since the start of 2024, the price of high-quality arabica beans, known for their smoother, less bitter taste, has surged by more than 100 percent. Meanwhile, robusta beans, typically used for instant coffee, have risen by over 90 percent (see chart 1). The primary culprit? The weather.

According to American author and environmentalist Edward Paul Abbey, “our culture runs on coffee and gasoline”, with “the first often tasting like the second”. While crude oil, the foundation of gasoline, has been trading in a comfortable range of USD 70 to 75 per barrel for months, the price of the coffee beans has been on a relentless upward trajectory.

Since the start of 2024, the price of high-quality arabica beans, known for their smoother, less bitter taste, has surged by more than 100 percent. Meanwhile, robusta beans, typically used for instant coffee, have risen by over 90 percent (see chart 1). The primary culprit? The weather.

Further upward pressure came from generally rising pro duction costs, including higher transportation and labor expenses. There were also reports that some farmers have been reluctant to sell their beans, speculating that prices will climb even further. More recently, geopolitical developments, such as Donald Trump’s (temporary) threats of sanctions against Colombia (which accounts for 8 per cent of global coffee production) have also played a role.

In response to soaring prices, major food companies have implemented price hikes. Despite this, demand for coffee remains strong. Coffee is either an essential daily staple or a luxury people refuse to forgo—depending on whom you ask. Unless harvests improve or consumers significantly cut back, the rally could continue for some time. For now, Brazil’s crop forecasting agency, Conab, expects the country’s coffee harvest to fall to 51.81 million bags in 2025/26—a 4.4 percent decline from the previous year.

However, the example of cocoa also shows that markets lose their appetite at some point, even for luxury goods: the commodity, which has been spoiled by success (strong rise in 2024), has already lost again a significant portion of its value in 2025 by early March.

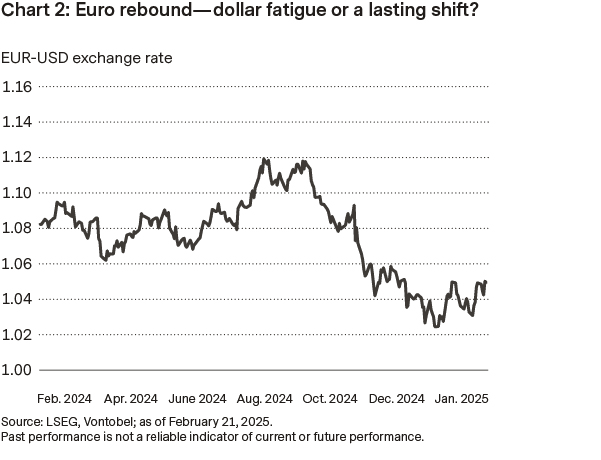

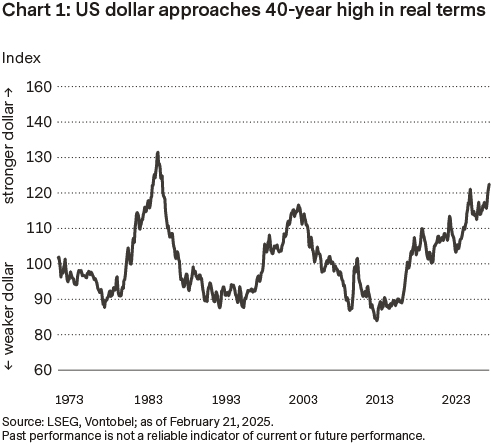

US dollar near 40-year high: strength or strain ahead?

The Trade-Weighted Real Dollar Index nears a 40-year high, driven by higher US interest rates, capital inflows, and safe-haven demand. After years of stability post 2008, the US dollar surged from 2015 onward as US yields outpaced global peers, reshaping trade and investment flows.

The index measures the dollar’s value against a basket of major trading partners’ currencies, adjusted for inflation, offering a more accurate picture of its purchasing power and competitiveness than nominal measures. Currencies from countries with significant US trade ties carry greater weight in the calculation. As chart 1 illustrates, the dollar has climbed steadily over the past decade. After remaining range-bound following the 2008–09 financial crisis, the dollar gained momentum from 2015, as the Fed raised rates while the ECB and Bank of Japan held policy rates near or below zero. Higher US yields made dollar-denominated assets more attractive, reinforcing its strength. With real dollar valuations approaching four-decade highs, the impact on trade, investment, and global financial stability is in sharp focus.

The dollar’s short-term trajectory remains closely linked to tariff policy developments. While a hardline stance has historically supported the currency, recent tough rhetoric is increasingly seen as strategic posturing, dampening its impact. Beyond trade uncertainty, economic fundamentals remain the strongest pillar of dollar strength. Optimism about US growth persists, but with the economy now in a later stage of the cycle, downside risks are higher than a year ago. Unlike early 2024, when skepticism prevailed, early 2025 expectations favor continued US dominance — leaving the dollar vulnerable to any signs of underperformance.

The euro’s rebound against the dollar (see chart 2) stems from a mix of factors, including dollar bull fatigue and lingering uncertainty around US trade policy. While tariffs remain a key risk, there is little clarity on how they will unfold. If Donald Trump’s proposed reciprocal, country-specific approach materializes, it could leave room for negotiation—potentially weakening the bullish dollar case. It’s too soon to call a lasting euro-dollar trend reversal, as the move appears more driven by dollar weakness than fundamental euro strength. Optimism over a potential Ukraine-Russia ceasefire is another factor that, if realized, could further support the euro. A stronger euro-dollar in a risk-on environment may also lift other currency pairs, with euro-franc among those poised to benefit.