The Defense Industry: A Turning Point Ahead?

For years, global disarmament has been a key focus on the international political agenda. However, geopolitical crises—particularly the conflict in Ukraine—have shifted the landscape and reignited demand for armaments. With the sobering realization of how fragile peace can be, calls for stronger defensive measures have increased. In response, several countries have announced investments in their defense industries and military capabilities to renew and modernize infrastructure that, in many cases, has become outdated.

NATO’s Role and the 2% Spending Target

The North Atlantic Treaty Organization (NATO) is one of the largest alliances of states in the world. For more than 80 years, NATO and the U.S. have played a crucial role in maintaining peace in Europe. However, since Russia’s invasion of Ukraine, the world has changed: peace has become more fragile and cannot be taken for granted. In addition, shifting political agendas and diverging national interests may cause some countries to reassess their security policies.

Even before taking office, U.S. President-elect Donald Trump urged NATO members to significantly increase their defense budgets. He has long criticized the failure of some countries to meet the so-called 2% target, accusing them of underinvesting in their defense infrastructure. This target, which requires each NATO member state to allocate 2% of its gross domestic product (GDP) to defense, was formally established at the 2014 NATO summit in Wales, influenced by Russia’s annexation of Crimea. The agreement also stipulated that countries not yet meeting the target should aim to do so within the next ten years.

While U.S. defense spending has consistently exceeded NATO’s benchmark, many European countries have fallen significantly short.

Increased Public Spending on the Defense Industry

Given the geopolitical fragmentation and ongoing international threats in various parts of the world, defense spending is expected to increase. In 2024, Europe’s defense industry recorded a 17% increase in revenue, according to the Aerospace, Security, and Defense Industries Association of Europe (ASD) This upward trend is likely to continue given the current geopolitical climate. Since Russia’s attack on Ukraine in February 2022, many NATO members have significantly increased their military expenditures. A recent NATO report highlights that in the current year, 23 out of 32 allies are expected to meet the 2% target this year. Germany’s military spending reached $61.1 billion in 2023, marking a 48% increase from 2022 and a 14% rise compared to pre-war levels. In 2024, for the first time, Germany’s defense budget is set to meet NATO’s target, with a calculated 2.12% of GDP—this was achieved partly thanks to a special €100 billion fund. However, in the coming years, the defense budget will need to increase significantly to sustain this level, keeping in mind that defense budget increases often take time to translate into operational impact.

Large Defense Companies in Europe

Amid increasing efforts to strengthen European defense and modernize military equipment, defense stocks have performed exceptionally well in recent years. SAAB, a leading Swedish company in aerospace, defense, and security, has tripled in value since Russia’s invasion of Ukraine. In addition, the general rise in defense spending within the European Union, recent developments in the President Trump´s trade war have led some of the U.S.’s trading partners to seek alternative suppliers for defense equipment.

SAAB offers an alternative to the U.S. F-35 fighter jet with its JAS Gripen, which may be of interest to both Portugal and Canada. However, SAAB is not the only major player in Europe, and competition remains fierce. While it is uncertain who will ultimately secure these potential orders, the growing interest in European alternatives highlights a broader shift that could continue to benefit the Europe´s defense sector. Nevertheless, some experts are raising concerns that SAAB’s valuation is becoming harder to justify than some of its competitors.

Related Products

Another large defense company in Europe is Rheinmetall. Although it operates in the same industry as SAAB, Rheinmetall has a broader portfolio. It has been one of the biggest beneficiaries of increased defense spending, securing large orders from the German government. Moreover, Rheinmetall is actively participating in collaborations with other defense companies to create a dominant force in European land defense systems, focusing on the industrial development and commercialization of next-generation combat vehicles. These efforts solidify Rheinmetall’s role in Europe's defense landscape, highlighting the shift toward regional cooperation and self-sufficiency.

Ultimately, while investment in the defense industry is likely to extend beyond Russia’s invasion of Ukraine, and some companies stand to benefit, markets often overestimate growth potential and inflate valuations. While this may not apply to the entire sector, it remains a key consideration, potentially suggesting increased volatility ahead.

The Importance of Aerospace Technology for Defense and Security Policy

The aerospace industry plays a crucial role in global defense and security policy. It includes the production of aircraft, satellites, missiles, and other airborne devices used for military purposes. These technologies, combined with airspace monitoring, are fundamental to maintaining an effective and credible defense. Ongoings technological advances and consistent infrastructure investments not only suggest military superiority but more importantly, serve primarily as a credible deterrent.

In addition, airspace is vital for surveillance and reconnaissance through satellites or drones—early detection of potential threats is essential for preventing major security issues. Reliable and secure communication, resistant to interception, is equally important for coordinating cross-border defense measures and conducting diplomatic negotiations. As space becomes increasingly critical to national security and defense, technologies to protect space assets becoming more important.

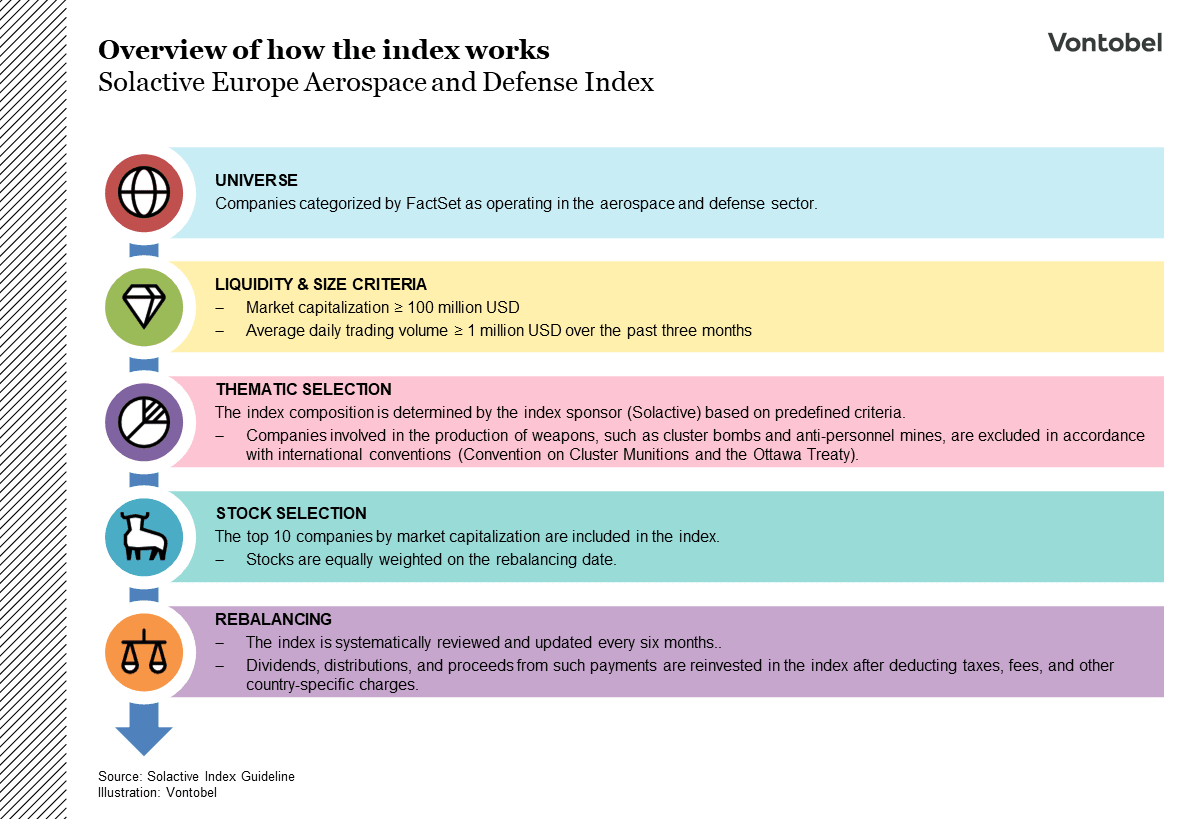

Overview of the Solactive Europe Aerospace and Defense Index

This brings us to the Solactive Europe Aerospace and Defense Index. Managed and calculated by Solactive AG, this index tracks the performance of a stock portfolio composed of companies active in the aerospace and defense sectors. Europe’s growing focus on this industry could drive the development and reinforcement of its defense infrastructure, thereby addressing existing investment gaps. As a result, the European aerospace and defense sector could offer attractive opportunities for investors. The need to revamp European defense capabilities could lead to increased investments in training, infrastructure, supplies, vehicles, and early warning systems. High technology and innovation are essential to advance military technology and ensure an efficient defense strategy. Moreover, the expansion of production capacity—along with the maintenance and replacement of aging infrastructure—could have a positive impact on sector´s growth prospects.

Related Products

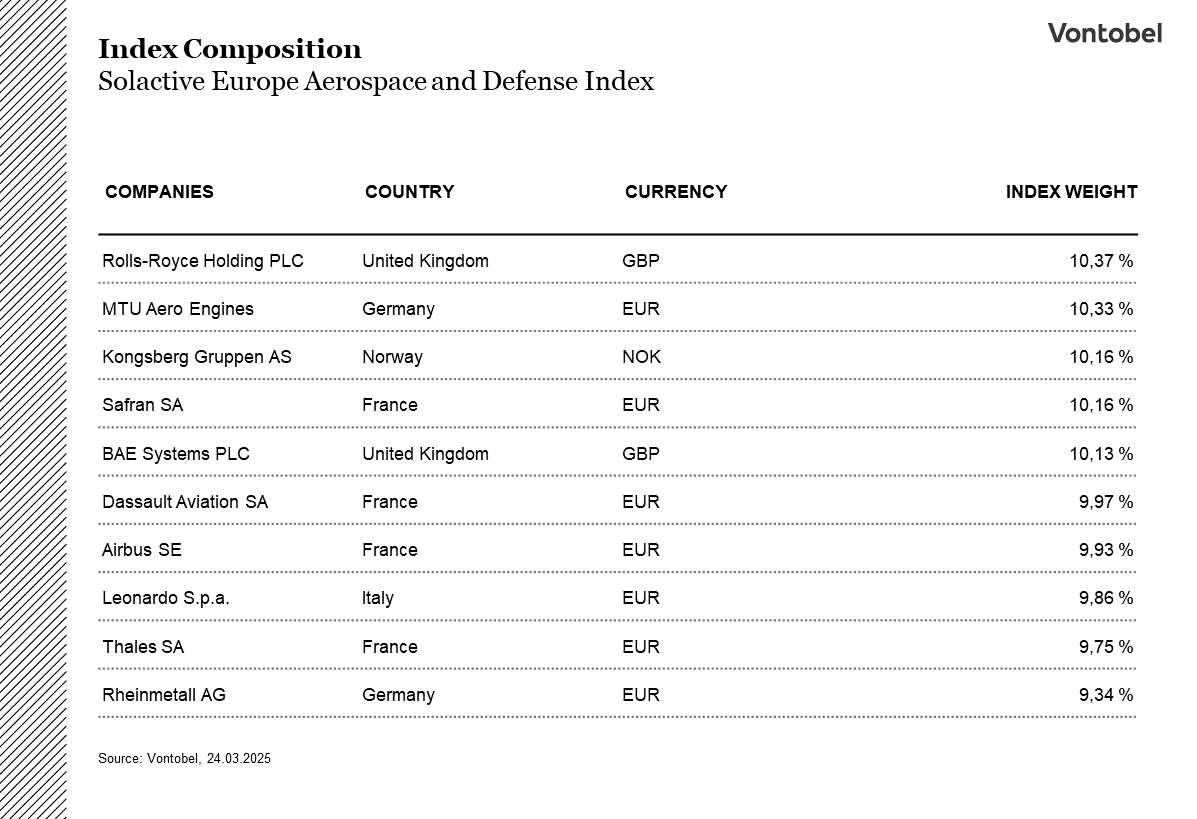

The tracker certificate on the Solactive Europe Aerospace and Defense Index allows investors to invest, with a single transaction, in the ten largest European companies by market capitalization operating in the aerospace and defense industry.

License Notice and Disclaimer

Solactive AG ("Solactive") is the licensor of the Solactive Europe Aerospace and Defense Index (the "Index"). Financial instruments based on the Index are not in any way sponsored, approved, promoted, or sold by Solactive, nor does Solactive provide any express or implied warranties, assurances, or guarantees regarding: (a) the opportunity to invest in such financial instruments; (b) the quality, accuracy, and/or completeness of the Index; and/or (c) the results that any individual or entity will achieve or may achieve through the use of the Index. Solactive does not guarantee the accuracy and/or completeness of the Index and assumes no responsibility for any errors or omissions related to the Index. Except for Solactive's obligations to its licensees, Solactive reserves the right to modify the calculation or publication methods related to the Index and assumes no responsibility for incorrect calculations or for incorrect, delayed, or interrupted publications related to the Index. Solactive is not responsible for any losses or damages of any kind, including any lost profits, business interruptions, or special, incidental, indirect, or other consequential damages arising from the use (or inability to use) the Index.

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.