European equities favoured despite Trump's tariffs

This week's case concerns the British Pound, which we believe has a good chance of strengthening against the US-Dollar (USD). This is against the backdrop of a weaker American economy, with President Trump's policies giving the US more inflationary impetus than is the case in the UK. Technical sell signals have emerged on several major equity indices. However, we believe that the momentum in favour of European equities relative to US equities could continue for some time.

Case of the week: Sterling may outperform the greenback

Since last September, the USD has enjoyed a monumental rally against most other currencies. When Trump was elected US President in November 2024, the US Dollar strengthened even further. Among the major currencies, the Great Britain Pound (GBP) has managed to hold a relatively large amount of ground against the USD compared to others. However, the USD has started to slide against the GBP since the beginning of the year. It is possible that the Cable will continue to strengthen in the coming months, as the US economy faces more inflationary pressures than the UK.

USD vs. major currencies indexed from 20 February 2024 to 20 February 2025, (USD baseline currency)

Since Trump entered the Oval Office, macroeconomic and currency markets have been in turmoil. What began as a great start for the USD has since become less stable and more fraught with uncertainty. Just in February, US non-farm payrolls came in well below consensus at 143k versus 170k expected. This was followed by a slightly lower unemployment rate of 4% versus the consensus estimate of 4.1%. This mixed bag of data was then further complicated by the following week's figures, namely the inflation rates for January. On a MoM (month-on-month) basis, core inflation came in at 0.4% versus the consensus estimate of 0.3%. On a YoY (year-on-year) basis, the figures were 3.3% and 3.1% respectively. As such, the uncertainty surrounding the state of the US economy is making things difficult for Powell. As Trump pushes ahead with tariffs and deportation plans, more inflationary pressures are likely to emerge as prices are artificially inflated by tariffs and low-skilled workers disappear, opening up jobs for locals with higher salary demands. At the same time, however, calls for interest rate cuts remain loud and frequent. So with the USD in disarray, investors looking at the currency may shrug their shoulders at all the uncertainty.

The GBP, on the other hand, has been a steady performer. The UK economy has been more consistent with figures coming in on the same side of the consensus line. The year-on-year inflation rate for January came in at 3%, compared to the consensus estimate of 2.8%. The core inflation rate on a YoY and MoM basis all came in higher than expected, as did the Producer Price Index (PPI) input and output data. At the beginning of February, the unemployment rate came in lower than expected and earnings were above the consensus estimate. This all points to a stronger than expected UK economy. This could lead to higher interest rates for longer, which in turn could strengthen the GBP against the USD.

GBP/USD seasonal pattern 2010-2025 YTD (year to date basis)

Looking at the seasonality of the GBP/USD, February has been a good month so far compared to the average. March tends to be a negative month, which means that if the seasonality holds, traders may want to time a long entry when the cable breaks above, for example, the third pivot support point at 1.256 GBP/USD. In the medium term, however, the British Pound looks set to outperform the USD. The risk is more bearish given the uncertainty surrounding Trump's policies. However, a risk-on currency trader could go long with a GBP/USD target of 1.27153, where the 3-10 day moving average crosses. Conversely, this would correspond to a target of USD/GBP 0.78645. An important short-term turning point will be the US economic data released on 28th February, when the Core PCE (Personal Consumption Index) price index, personal income and personal spending will be published. If these figures point to a weaker US economy, the stage will be set for a long cable play.

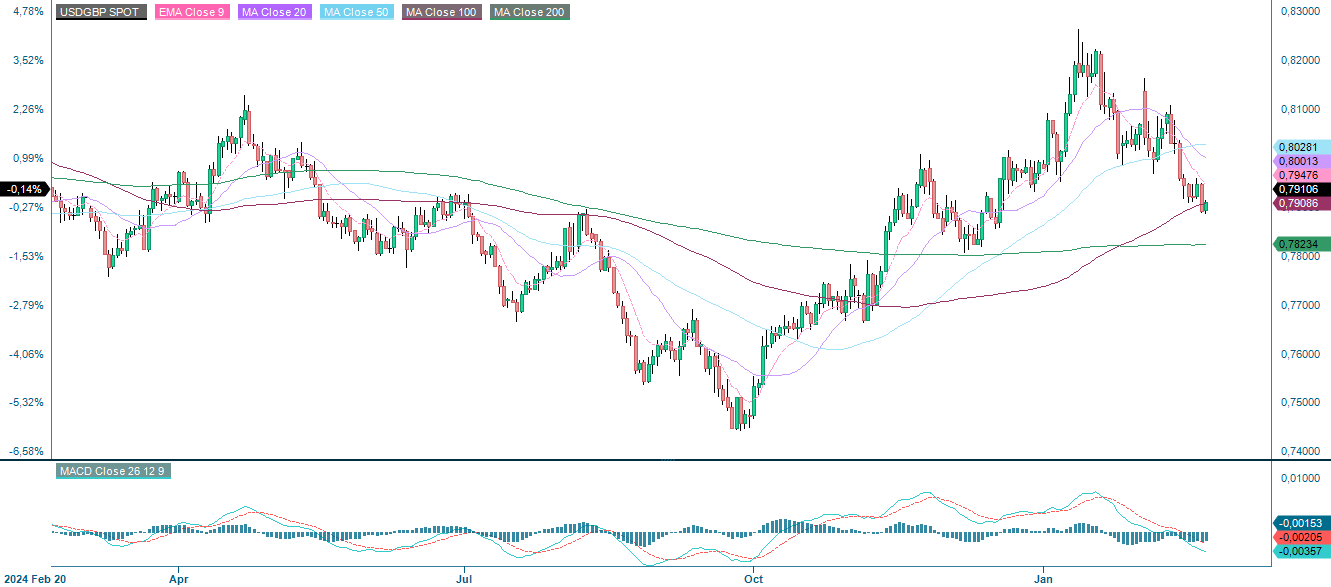

USD/GBP spot price, one-year daily chart

USD/GBP spot price, five-year weekly chart

Macro comments

US equity markets fell sharply on Friday 21 February, ending last week in negative territory. The S&P 500 closed down 1.7%, the Nasdaq down 2.1% and the small-cap Russell 2000 was down 2.9%. The Magnificent 7 contributed significantly to the declines. Tesla was down 4.7%, Nvidia fell 4.1%, Amazon was down 2.8% and Alphabet fell 2.7%. US consumer confidence was weaker than expected according to the Michigan index for February, which fell to 64.7 from 71.1 in January. A drop to 67.8 had been expected. Friday's flash purchasing managers' index (PMI) for February was in line with expectations, while the services PMI was much weaker than the consensus estimate at 49.7 versus 53 expected.

As shown in the chart below, which ranks the performance of the world's major stock indices, European stock markets have shown strong momentum so far in 2025. The worst performing index is the US small-cap Russell 2000, which includes companies that investors believed will benefit most from Trump when he was elected US president in November 2024.

Year-to-date (YTD), one-year and five-year performance of equity indices ranked on a YTD basis

Later today, Wednesday 26 February, Nvidia will release an interim report that could be important for the stock market. The macroeconomic calendar starts at 8.00 CET (Central European Time) with the Swedish PPI for January and the German Growth from Knowledge (GfK) Consumer Confidence for March. This is followed by the French Household Confidence Indicator for February at 8.45 CET. From the US, we get New Home Sales for January and Oil Inventories (Department of Energy), weekly statistics.

On Thursday the 27th we start with the Swedish Trade Balance for January. From Spain we get the CPI (Consumer Price Index) and from the Euro-Zone the economic barometer, both for February. The minutes of the ECB (European Central Bank) meeting on 30th January are also due. From the United States, we get January Durable Goods Orders, Q4 GDP (Gross Domestic Product), Initial Jobless Claims as well as January Contracted Home Purchases and the February Kansas City Federal Reserve (Fed) Index.

On Friday, 28th February, the macroeconomic agenda starts at 0.50 CET with Japan's Industrial Production for January. At 8.00 CET we will get Sweden's Q4 GDP as well as Germany's January retail sales and import prices. France's February CPI and Q4 GDP will follow 45 minutes later. Germany's unemployment rate for February is due out just over an hour later. Around lunchtime we get Italy's and Germany's CPI for February. Then we move to North America with Canada's Q4 GDP and from the United States, private consumption and inflation (PCE), goods trade balance and inventories of unsold goods, all for January. Finally, we have the Chicago PMI for February.

Short the US and long Europe may continue to be the trade of choice

The S&P 500 is under pressure as the index is currently trading below a support line consisting of a MA100. Note that the MACD is about to give a sell signal. The next level on the downside is at 5,865. As the index has bounced around this level on several occasions, it could be an opportunity for the brave to make some small purchases.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The Nasdaq 100 is currently trading at support. A break below and levels around 20,785 could be next. The next level on the downside is around 21,030 where the MA100 meets.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

Meanwhile, the Swedish OMXS30 appears to be trading in another bullish flag formation. A break to the upside and 2,800 could be next. However, the break must come relatively soon. Also note that the MACD has generated a soft sell signal.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The MACD has given a clear soft sell signal for the German DAX and the index is consolidating near the support formed by EMA9. The next level on the downside is around 22,100 where MA20 meets. Nevertheless, as money continues to flow into European equities, going long Europe and short the US could remain a winning trade for some time.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.