US tech companies enter Q4 earnings season

The US technology sector fell by 5.6% on Monday 27th January, driven by Artificial Intelligence (AI) related companies with a focus on Nvidia. Investors were concerned about the strong characteristics that the Chinese DeepSeek model appeared to have, given Nvidia's heavy reliance on GPU (Graphics Processing Unit) sales. However, we believe that the fall in Nvidia's share price is an overreaction that could create buying opportunities for bold investors. The focus on the US tech sector is likely to intensify as Meta Platforms, Microsoft, Apple and Tesla report their Q4 results this week.

Case of the week: Nvidia, AI sell-off creates opportunities for bold investors

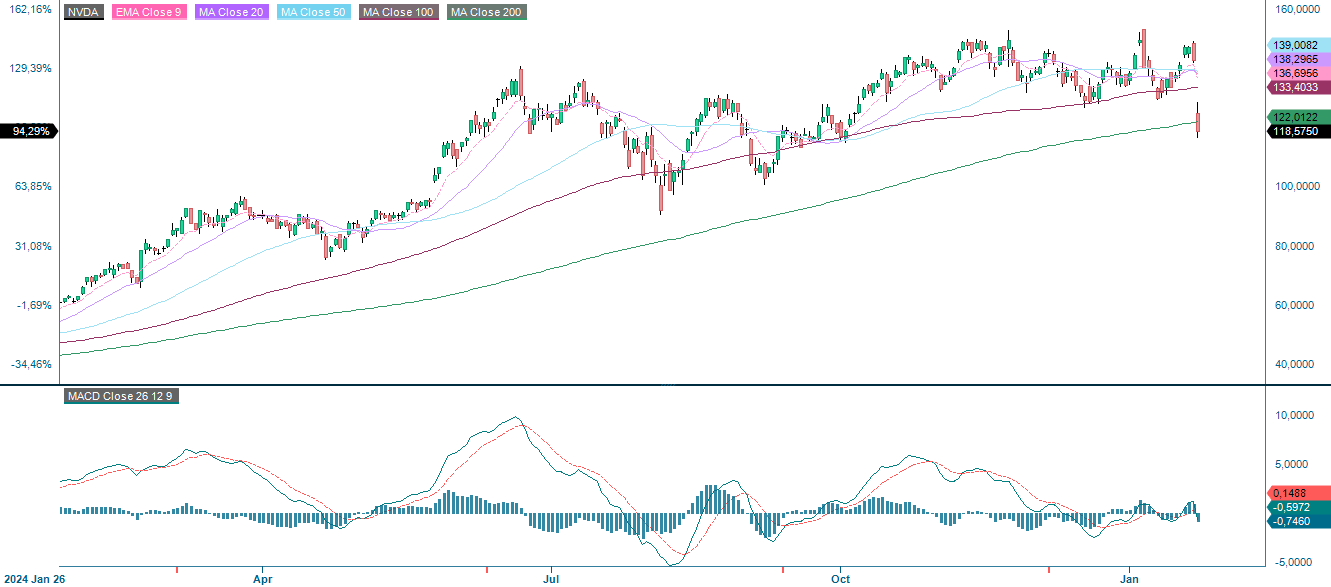

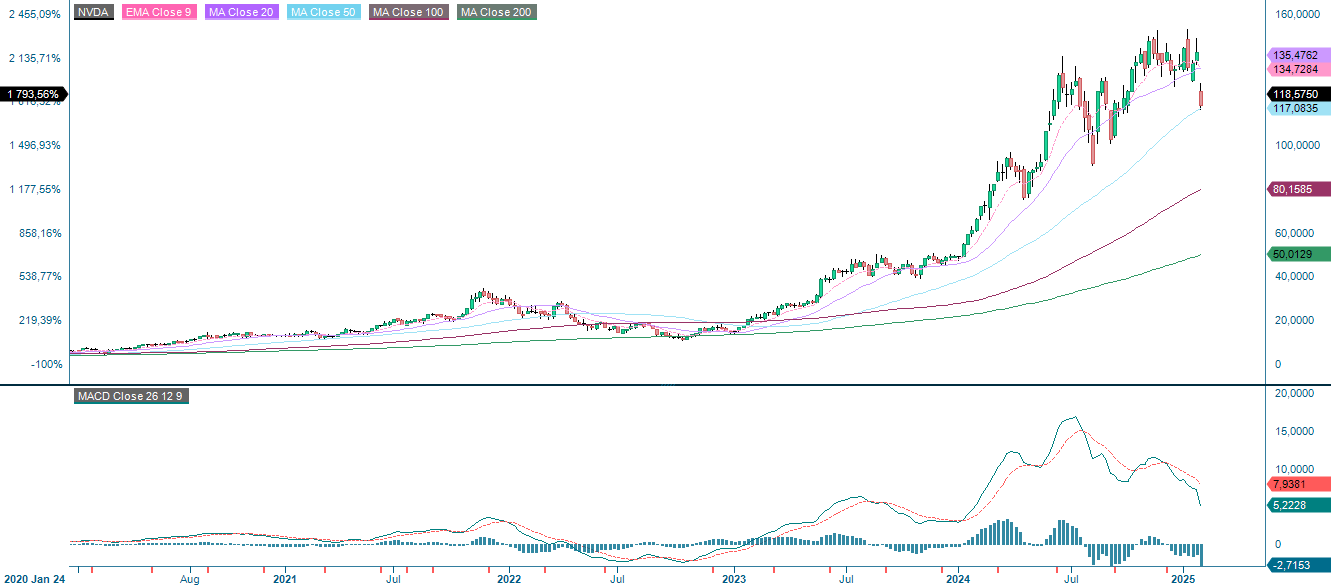

Nvidia Corporation ("Nvidia") experienced a significant sell-off on Monday 27th January following reports that China's DeepSeek had demonstrated strong performance for its new large language model (LLM), reportedly achieved on a limited budget and without access to Nvidia's high-end GPU accelerators. This development has raised investor concerns that DeepSeek's success could weaken Nvidia's pricing power and prompt hyperscale cloud providers to scale back their AI-related spending.

It seems that the AI boom - at least as far as the stock market is concerned - has encountered its first significant challenge. Just as investors had become convinced that advanced AI was dominated by American companies - with hyperscalers investing more in AI than entire nations, OpenAI unveiling new models at a rapid pace, and Nvidia providing the GPUs that power these breakthroughs - a relatively small Chinese company has emerged to disrupt the established order.

While the market's reaction is somewhat understandable, given Nvidia's heavy reliance on GPU sales to maintain its dominance in AI, it's important to question whether these fears warrant such a dramatic sell-off. For starters, DeepSeek's touted cost efficiency and performance have yet to be rigorously validated. Early announcements of new technologies often generate excitement, but scaling them up into reliable, practical solutions is a much bigger challenge. Nvidia's GPUs, such as the H100 and A100 series, are widely regarded as the industry standard for AI development due to their unmatched performance and integration with a robust ecosystem of AI tools. It's unlikely that a newcomer could disrupt Nvidia's deeply entrenched position without significant time, resources and innovation.

In addition, geopolitical factors could severely limit DeepSeek's ability to gain traction in global markets. US trade restrictions on Chinese AI technologies and products could limit the export of DeepSeek's solutions to key Western markets. As a result, DeepSeek's influence is likely to remain limited to China, a market where Nvidia already has a strong position and even offers custom-designed chips to comply with local regulations. These dynamics significantly reduce the potential threat from DeepSeek.

Nvidia's success is not just tied to its hardware sales. Its software ecosystem, such as CUDA, as well as its AI-focused platforms and cloud solutions, provide the company with a significant competitive moat. In addition, Nvidia continues to invest heavily in the development of next-generation technologies, ensuring it stays ahead of the curve in an industry that prioritises innovation.

While it is prudent for investors to pay attention to emerging competitors, the sell-off reflects a disproportionate reaction to a speculative risk. Nvidia's fundamentals remain exceptionally strong, supported by its diversified revenue streams and the ongoing global adoption of AI across industries. Nvidia's long-term growth prospects are further underpinned by trends such as autonomous vehicles, the metaverse and edge computing, all of which require powerful computing capabilities.

Investors could view the recent dip in the share price as an overcorrection, potentially offering an opportunity for long-term gains. Fears surrounding DeepSeek are likely to subside as more realistic assessments of its impact emerge. Nvidia's track record of dominating the AI space, combined with its strategic adaptability, suggests the company is well positioned to overcome challenges and continue to drive growth in the years ahead.

Nvidia (USD), one-year daily chart

Nvidia (USD), five-year weekly chart

Macro comments

The euro area composite PMI (Purchasing Manegers’ Index) rose to 50.1 in January from 49.5 in December. In the US, the composite PMI fell to 52.4 from 55.4. On a positive note, the US manufacturing sector rebounded to 50.1 from 49.7 expected, while the services sector lost some momentum (52.8 from 56.5 expected). Hopes of tax cuts and deregulation continue to fuel optimism in the US economy. Continued weakness in Eurozone PMI data has been a key argument for the European Central Bank (ECB) to cut interest rates, with a rate announcement expected on 30 January. The market expects further rate cuts from the ECB in 2025. The Federal Reserve (Fed), which makes its next interest rate announcement today, Wednesday 29th January, is expected to remain on hold on interest rate changes due to the relative strength of the US economy.

For the fourth quarter of 2024 (with 16% of S&P500 companies reporting on Friday 24 January), 80% of companies have reported a positive EPS (Earnings Per Share) surprise, while 62% of companies have reported a positive revenue surprise, according to Earnings Insight.

Eleven US companies with a market capitalisation of at least 10 billion US dollars that reported last week beat analysts' earnings estimates by an average of 9.8% and a median of 2.0%. The average share price of these companies rose by 2.1% and the median by 1.9% one day after the release of their Q4 reports.

Q4 earnings estimate vs actual, deviation (in %) for US companies

US tech companies start to report this week, with Microsoft, Meta Platforms, ASML Holding, Automatic Data Processing, IBM, Tesla and T-Mobile US reporting on Wednesday 29 January, along with Danaher, Lam Research, The Progressive and ServiceNow. From an OMX perspective, it is also a busy day with Q4 reports from SEB, SSAB, Tele2, Volvo and Trelleborg. In Asia, Alibaba is due to report. Wednesday's macroeconomic releases include German GfK (Gesellschaft für Konsumforschung) consumer confidence for February and Spanish Q4 Gross Domestic Product (GDP). During the day, we will see interest rate announcements from the Swedish Riksbank, the Bank of Canada and the Federal Reserve. From the US, we also get the December trade balance and wholesale inventories as well as Oil inventories (Department of Energy), weekly statistics.

The US earnings season continues on Thursday 30th January with Apple, Caterpillar, Cigna, Comcast, Intel, Mastercard, Thermo Fischer Scientific, United Parcel Service and Visa reporting. In Europe, Deutsche Bank, Roche Holding, Sanofi and Shell are due to report, while in the Nordics ABB, Electrolux, Epiroc, H&M, Kone, Nokia, Nordea and Telia are on the calendar. Macro news kicks off with France's Q4 GDP, followed by Sweden's December retail sales. Q4 GDP is also due from Italy, Germany and the Eurozone. Spain will release Consumer Price Index (CPI) for January and we will also get a Eurozone economic barometer for January as well as an ECB rate announcement. The US will release Q4 GDP and initial jobless claims.

The macro agenda for Friday the 31st starts with Japan's unemployment rate, industrial PMI and retail sales for December. From Europe, we get German retail sales and import prices for December, as well as unemployment and CPI for January. We also get January CPI from France, as well as household inflation expectations in the euro area. Turning to North America, we get Canada's GDP for December as well as Q4 labour costs, private consumption, inflation (Personal Consumption Expenditures, PCE) for December and the Chicago PMI for January from the United States. On Friday, we await interim reports from Exxon Mobil, AbbVie and Chevron in the US, from Novartis in Continental Europe and from Autoliv, Elisa, ELUX PRO, Hexagon, Holmen, SCA and SKF in the Nordic region.

DAX index composition may be attractive to bubble believers

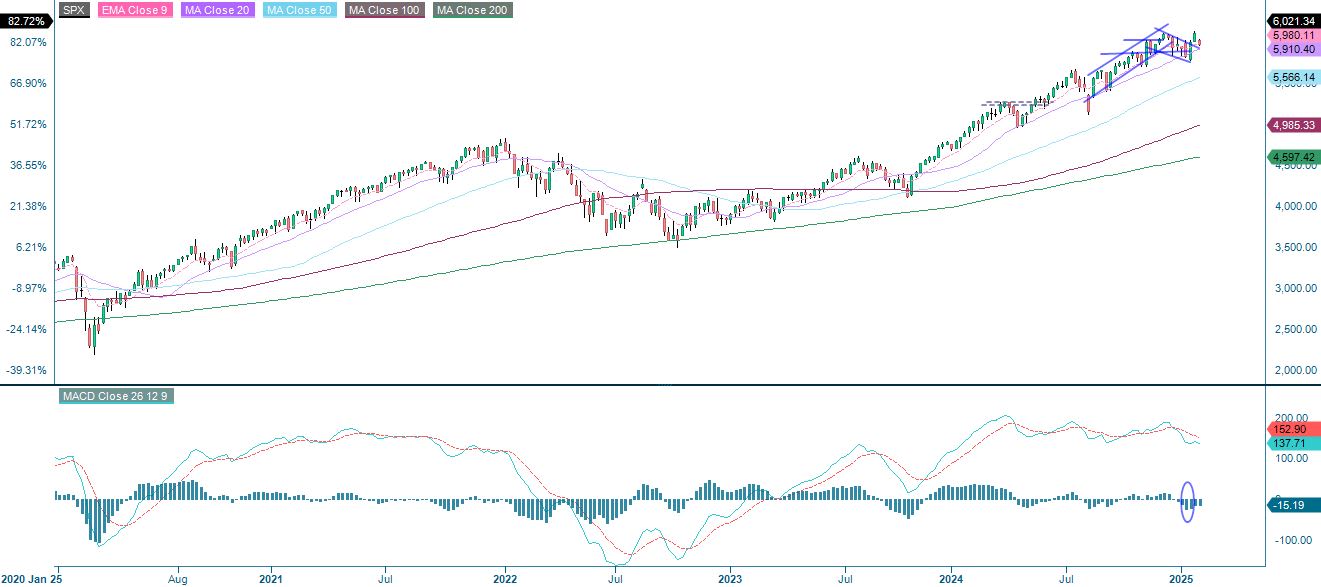

The S&P 500 is currently trading above the MA20, which is acting as support on the downside. It will be interesting to see if Monday's gap can be closed. If the sell-off regains momentum, MA100, currently at 5,878, could be next.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The tech-heavy Nasdaq 100, on the other hand, has broken below its MA20 and the downside risk is still very much present. The next level on the downside is 20,613 where the MA100 meets.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

The German DAX is less exposed to a potential AI bubble due to its index composition. Nevertheless, sentiment in the US is reflected in trading in Europe. It is not unlikely that the DAX will need help from across the ocean to make new highs. On the other hand, note that the Relative Strength Index (RSI) is showing overbought levels. In a scenario where the momentum turns south, the first level of support is the EMA9 at 21,130, followed by the MA20 at 20,629.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

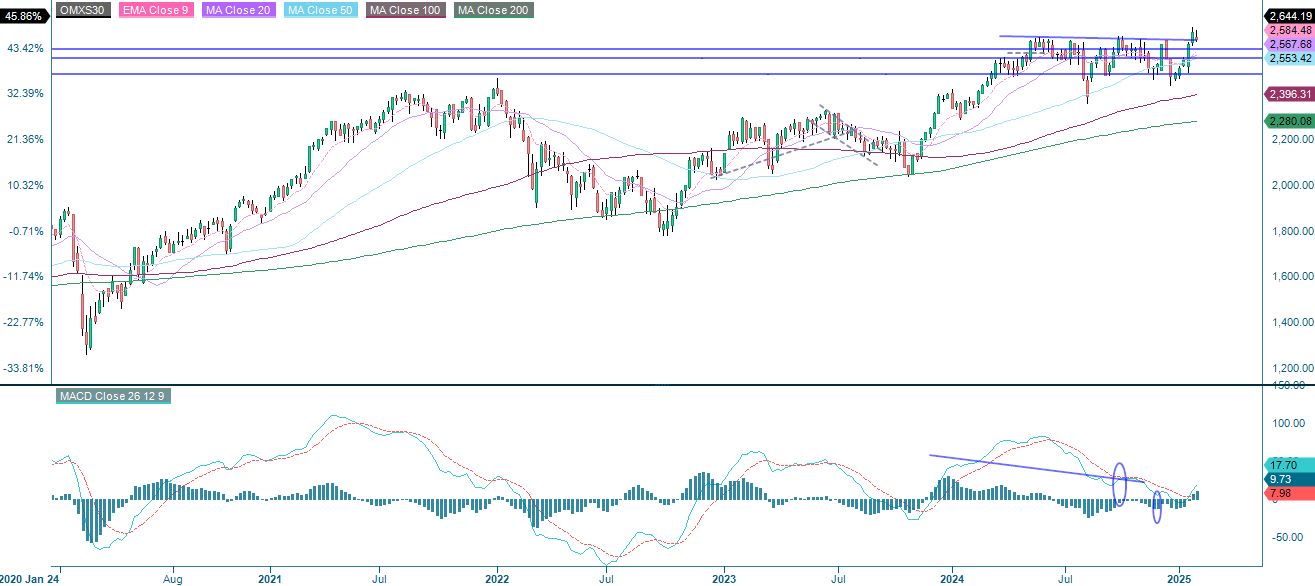

The OMXS30 is currently trading at a support level. Tuesday's intraday trading appears to have been weak as the index briefly filled the gap before retreating again. Like the DAX, the OMXS30 may need the AI bubble concerns to subside to some extent.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.