Higher bond yields weigh on equity markets

Tight cattle supply due to increased production efficiency, combined with a normal rise in prices during the spring season, makes the outlook for the first half of 2025 promising in this defensive case. The US Department of Agriculture (USDA) also lowered its 2025 beef production forecast in December. Further gains in equities are currently being held back by higher US and German government bond yields. Our technical analysis shows a sell signal on the MACD for the S&P500, while the DAX continues to show strength.

Case of the week: Live cattle look promising for 2025

At the start of 2025, cattle prices have continued to rise on the back of tight supplies and Trump's victory in the US presidential election. Since the dip in late summer last year, prices have been above the previous All Time High (ATH). As discussed in our last case on cattle in August 2024, the typical seasonal pattern is for prices to rise in the spring and peak during the summer barbecue season. As summer gives way to autumn, prices fall as lean hogs increase. However, in the fourth quarter, live cattle prices have risen while hog prices have fallen. The cattle cycle, as described by the CME Group, suggests that prices will remain elevated into 2025 as supply takes time to readjust to demand. The case is further strengthened by the discovery of New World screwworm in cattle in Mexico, which has led to a ban on cattle imports from Mexico.

While prices did rise sharply in late September, as we predicted in early August, they did not spike. Instead, prices remained flat until the end of December, when they rose again above USD 190 per pound. As of early January 2025, prices have now breached the $195 mark, surpassing last year's ATH. As livestock-related fixed prices have risen over the past 12 months and demand for beef has increased, supply has been tightened. The reduced number of animals is partly because cattle farming is more efficient than ever. Cattle now live an average of 468 days compared to 609 days in 1977. In addition, the average carcass yields 28% more beef than before, meaning that the same amount of beef can be produced with 69.9% of the animals and using only 81.4% of the feed. However, despite the improvements in efficiency, supply is struggling to meet demand, a phenomenon that could be explained by the cattle cycle.

The cattle cycle, typically 10 years from peak to trough, has been documented since 1890. During this period, 12 peaks and 11 troughs have been observed. In terms of cattle numbers, the 2014-2024 cycle is in line with previously observed contraction cycles.

Cattle cycles compared from 1979 to date

When the contraction cycle will end remains to be seen, but it is safe to assume that as long as the number of cattle continues to fall, prices will not do the same, barring freak weather events or exogenous demand shocks. This trend is further reinforced by the ban on Mexican cattle imports. The ban, introduced in November, was confirmed to remain in place in December as the USDA backtracked on earlier comments that it could resume imports of Mexican cattle before the year-end holidays. Dr Rosemary Sifford, the USDA's chief veterinary officer, said that "shipments are likely to resume gradually after the first of the year, with a full resumption of live animal movements thereafter". However, at the time of writing, there has been no update on whether shipments have resumed. In any case, the ban, albeit temporary, has not helped to boost cattle numbers. According to the USDA's December outlook, projected beef production in 2025 was cut by 615 million pounds compared to the November forecast. The new forecast is for 25.665 billion pounds of beef to be produced in 2025. If demand remains flat, it is likely that imports will have to increase to make up for lost production, potentially pushing prices even higher.

Taken together, it is possible that resumed imports from Mexico could temporarily dampen futures prices. However, it seems unlikely that futures prices will remain subdued for long. Price headwinds include the current stage of the cattle cycle, less-than-ideal weather, expected Trump tariffs that will hurt imports, and the typical seasonality of prices rising as grilling increases. Thus, an investor could potentially enter the commodity by going long after a temporary dip caused by resumed imports from Mexico.

Cattle (USD/Lbs), one-year daily chart

Cattle (USD/Lbs), five-year weekly chart

Macro comments

After a very strong year for equity markets in 2024, there was no energy left for a December rally. Equity markets have also had a weak start to 2025, which is usually a seasonally strong period. One possible explanation is that US and German ten-year government bond yields have risen by 48 and 42 basis points respectively over the past month.

On Thursday, 9th January, the macroeconomic calendar kicks off with German Trade Balance, Industrial Production and Machinery Orders for November. From the Euro-zone, we have Retail Sales for November. From the US, we get the Challenger Job Cuts reports for December and Wholesale Inventories for November. On Thursday, Tesco and Fast Retailing will also release their interim results.

First, on Friday morning, 10th January, we get Japanese household consumption for November. About seven hours later, Statistics Sweden presents a Gross Domestic Product (GDP) indicator, industrial orders and household consumption for November. France will release industrial production for November. The most important figure on Friday will be the US non-farm payrolls for December. The result for November was 227,000 new jobs, of which 194,000 were in the private sector. Expectations for December are for 154,000 new jobs, with the private sector expected to contribute 130,000 new jobs. From North America, we also get Canada's employment for December as well as the Michigan index for January from the U.S. On Friday, we also get interim results from Walgreens Boots and Delta Air Lines.

US nonfarm payrolls, January 2023-December 2024

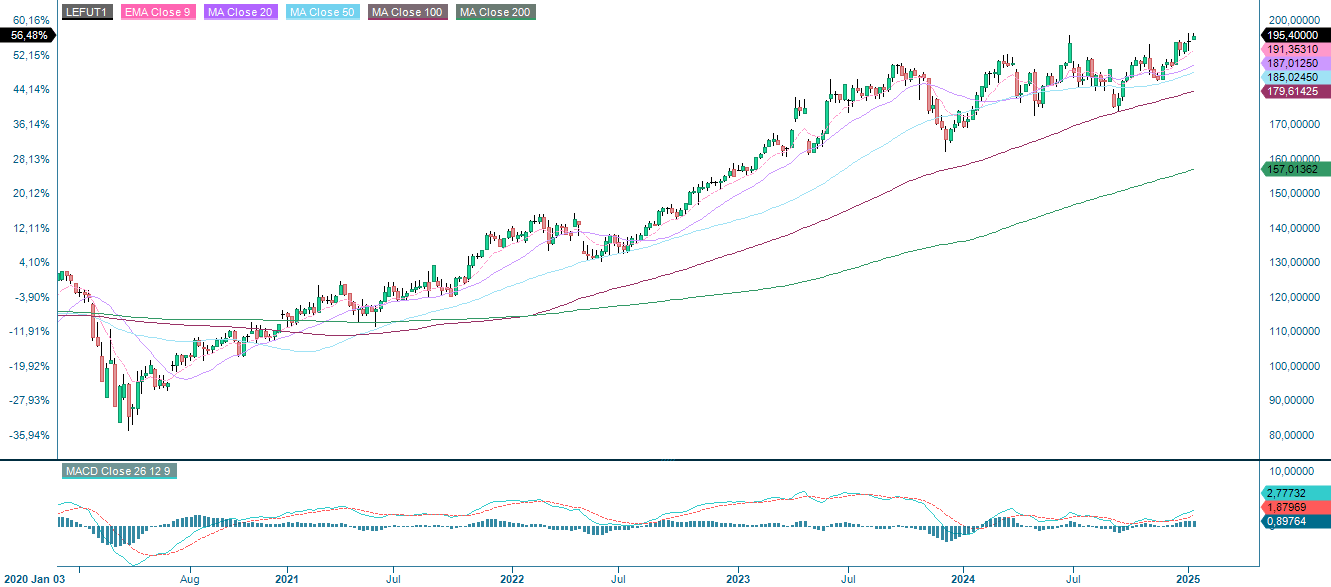

US equities under pressure – will the DAX follow?

US equities are under pressure. Rising yields are not helping. As the chart below shows, the S&P 500 is currently trading at support at 5,875. The MACD has given a sell signal and the next level to the downside is the MA100, currently at 5,825. Support is found on the weekly chart at 5,840. For the adventurous, dips below this support could be a buying opportunity.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

Meanwhile, the Nasdaq 100 is trading at a support formed by the MA50 currently at 21,065. Note that the MACD is approaching a sell signal. A break to the downside and 20,660 could be the next target.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

The DAX, on the other hand, has shown strength and is back around the previous high. But given the sentiment in the US, will the DAX follow? A break below the MA20, currently at 20,190 and levels around 19,820 could be next.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

The OMXS30 is trading just below resistance, which is a cluster of moving averages. If the weak momentum from the US spills over to Europe, it is not unlikely that the OMXS30 will return to the 2,500 level.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.