Navigating extremely stormy waters to your advantage

It's different now. It's fun because it's actually true. I know, the memo has had its own life now. After all, we have learned that it is never different, that nothing is new under the sun, that countries with excessive debts never repay honestly. Reinhart and Rogoff showed it in an attention-grabbing report a few years ago. But the first half of 2020 has surprised so many that many are now competing to guess more unexpected events that would take place this year.

It's different now. It's fun because it's actually true. I know, the memo has had its own life now. After all, we have learned that it is never different, that nothing is new under the sun, that countries with excessive debts never repay honestly. Reinhart and Rogoff showed it in an attention-grabbing report a few years ago. But the first half of 2020 has surprised so many that many are now competing to guess more unexpected events that would take place this year.

Legendary investors such as Howard Marks and Jeremy Grantham have gone so far that, without irony, they dare argue that 2020 is nothing like anything else. The combination of historical records in the form of a pandemic, recession, bankruptcies, number of new unemployed, debts for companies and states, valuation levels, money printing, universal basic income, oil price movements (minus $ 40 per barrel) means that previous extreme market situations cannot be used as templates. It is not even possible to use some kind of weighted average of these to make predictions about the outcome. The global economy is simply too complex to calculate how billions of newly printed dollars will interact with a 99 percent decline in air travel and 40 million newly registered unemployed in the United States.

Right now, the US central bank is trying to create peace and quiet by stretching out a safety net under the financial markets. They think that as long as no one can lose money on their financial instruments, the mood is kept up by employers, contractors, customers and the unemployed. Perhaps the worst thing about the Covid disaster is that it struck when world trade was already on the downturn at the same time as both the stock market valuations and debt holdings of companies and states set historical records. The downturn of the economy then created both a supply and a demand shock and that is precisely what makes a broad V recovery for the economy virtually impossible. Central banks and other politicians can stimulate and simulate higher demand, but the supply side is more difficult to do something about. Some service industries are still closed and many companies that went bankrupt will not start in a while. How would you do if your restaurant went bankrupt?

The situation is extremely uncertain, and not even the most savvy economic thinkers and managers dare say whether we will see a wave of consumer price inflation or debt and price deflation, or if the dollar will strengthen sharply or on the contrary fall significantly against other fiat currencies. I myself cannot set foot on whether the stock market could be doubled or halved. Many, and I'm probably also in that camp, often say that it will be both, but there is disagreement about the order in which it may happen: first stocks go up 100% and down 50% later, or vice versa? Firtst there is deflation followed by inflation? First the dollar prevails and then crashes?

I like to look at the world quite easily. When a record amount of money is printed, I want gold in various forms, for example physically and in the form of mining shares, but also various exchange traded products work well. Crypto currencies are interesting for the same reason - partly as an inflation hedge, and partly as a way of withdrawing from the central banks' increasingly eroded and empty systems. In addition to Bitcoin, there is also Ether, which in turn can also be said to give exposure to a general technological development, which I, Anna Svahn and Eric Wall have given some thought in some sections of the podcast "outsiders". Agricultural commodities also fit into these ideas of not only protecting themselves against the desperate measures of central banks, but even taking advantage of them in various ways.

Mini Futures

When the money supply is unrestricted, the economy gradually becomes less efficient. The price signals that control the allocation of resources in society work worse and the tendencies to engage in financial speculation rather than efficient production are reinforced. Stock prices are also naturally lifted by access to more money, but as the economy and companies are basically getting worse, prices of actual real assets such as gold and crypto are raised even more. In addition, gold is lifted from an undervalued level and has a period of catching up with the money supply first and then further benefiting from the continued increase. This year, moreover, the flow into gold-backed ETFs has set a new annual record, after only five months. The central banks also buy gold with both hands as insurance against their own policies and as bargaining chips when the global fiat system has to be rebuilt from the ground up due to completely unsustainable debt levels and promises of spending to citizens.

The cryptocurrencies, for their part, are proving how large a share of the economy they can represent, which means that we can face a real paradigm shift in the financial field. In that scenario, there is nothing else that can compete with Bitcoin and Ether in the 10-year term, just as nobody could compete with them for the past ten years either. Well, nothing new on the horizon there either, but just more of the same from the last decade.

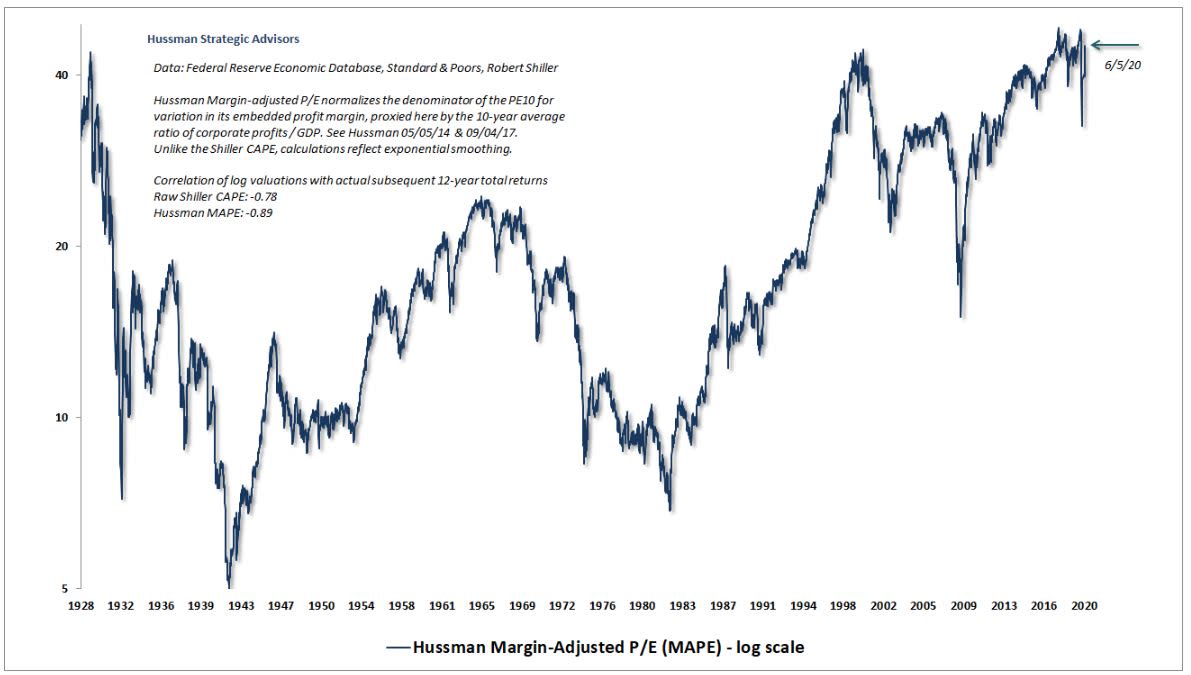

You can't eat Price-to-Earnings (P / E) numbers, I usually say. You can only eat the underlying value creation. In the short term, however, new money can always raise worthless shares in insolvent companies, or just raise the price and P / E ratio in companies, whether their profits grow or not, or even exist. And, yes, you can always believe in and hope that a constantly accelerating inflow of more and more useless fiat money from central banks will lift all boats, and that P / E 45 (today's adjusted PE number [MAPE] for the S&P 500) can thus become 60, 75, 90 and 100 in the long run. But then you can never relax, because if 100 money only buys you 1 in earnings then you have to sell the share to someone else when you buy real things. You can't eat the P / E figure no matter how high it is, you can only eat the underlying result or another's stock buyer's 100-note which in turn must be hoping for a buyer.

Source: Hussman Strategic Advisors

In my world, I would rather look for value-based themes, forgotten and profitable islands of real value, of P / E = 10, i.e. a kind of promises of annual returns of around 10%. I think this is a reasonable compensation for my time, money and effort over a year. It is even a requirement. In addition to requiring 10%, I also believe that I can always find such alternatives. When 20% new money is printed per year eg. then gold implicitly yields something similar. When a promising tech company trades at P / E = 10 in five years and with continued high growth, it also gives me about 10% on average annual compensation for my risk-taking and deferred consumption. Maybe the FANG shares are value plays. Perhaps. You can count on that yourself. But the whole stock exchange is not, not at MAPE = 45.

The world is more uncertain than ever, while totally inexperienced and insecure Robinhooders call history's best investor Warren Buffett passé, when they invest their salaries in buy options and insolvent companies instead of betting on sports. And it has worked. In the short term, with Jay Powell's Fed in their corner, they have struck hedge funds and big banks with horse lengths. But in the slightly longer term, the Ponzi strategy does not hold. The question is what you as a thinking investor can do more than the ideas above about gold, crypto and smart value, to become a winner when the whole sea storms.

Diversification between uncorrelated asset classes is the only free lunch on the financial market, I usually say. It is easy to show that a portfolios of stocks and gold, or stocks, gold and agricultural commodities, or all of these plus cash or bonds, have a better return per volatility unit than the different asset classes individually. Diversification is a way of keeping “dry powder” ready for future battles, while still having the money to work in any market. With a portfolio that also includes assets such as gold and cocoa, you dare to mix both momentum shares, deep value, smart (growth) value and long-term attractive themes such as 5G, Industry 4.0, fish farming or food deliveries, despite generally sky-high values and weak finances.

Tracker Certificates

When the tug-of-war between new money and a pale economic reality is extra intense, interesting opportunities arise more often than usual. Embrace that we live in extremely interesting times and at the same time the most democratized financial market ever. Everyone has access to a free online broker and an endless amount of free information and inspiration for their investments on the internet. It creates a special dynamic in the market with unmotivated price movements more often than before. However, the more error pricing, the better for anyone who can keep their heads cold and combine momentum and value on the stock side with well thought out rebalancing schemes in other asset classes such as gold and crypto.

@Mikael Syding

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.