Big in Japan: return of inflation opens up new investment opportunities

After decades of stagnating prices, Japan seems to have found its way back to inflation. This changed environment of monetary policy normalization and slightly positive inflation is having a positive effect on the Japanese stock market and is also attracting foreign investors again. For this reason, Japanese companies could play an increasingly important role in global portfolios again in the future.

For a long time, investors avoided Japan, the "Land of the Rising Sun". The reason for this was that the macroeconomic environment appeared unattractive due to low growth and the prevailing deflation. The country was heavily influenced by the severe previous crises in the 1990s and 2000s. When the so-called "bubble economy" burst in the 1990s, the NIKKEI 225® lost almost two-thirds of its value two years later and has still not reached the highs of 1989. Economic development from the 2000s onwards was very weak and characterized by the deflation that began in 1998. For this reason, there is also talk of two lost decades.

Changed situation in Japan's economy

However, the situation in Japan appears to have changed fundamentally. While many countries are still struggling with excessively high inflation rates, the Japanese economy, on the other hand, is delighted with the return of rising prices in its own country. After almost two decades of stagnating prices, they finally seem to have found their way out of the tight corset of deflation. Accordingly, the slightly positive inflation now appears low and even attractive by international standards.

In this new, changed macroeconomic market environment, the Japanese stock market appears to be making a new advance and at the same time attracting more foreign investors. The Japanese share index, Nikkei 225, has risen by 22.88% since the beginning of the current year (as at 01.11.23) and is now at its highest level for 29 years. This performance also puts the Japanese stock market well ahead of its international competitors. The performance to date shows how attractive the Japanese stock market appears to have become again recently. However, instead of investing directly in the very broad, price-weighted NIKKEI 225 price index, it could be interesting for investors to invest in a few selected companies.

The Japanese benchmark index: Tokyo Stock Price Index (TOPIX) or NIKKEI 225

In contrast to the NIKKEI 225, the TOPIX, with its almost 2000 companies, provides a more accurate picture of the Japanese stock market as a whole. The weighting of the individual companies in the TOPIX is based on their market capitalization. The calculation of the TOPIX was started back in 1968 - at that time the index started at 100 points and is often used for trend analysis and as a benchmark. This is one of the reasons why professional investors often rely on the TOPIX, while the NIKKEI 225 dominates media coverage. With only 225 companies, the NIKKEI 225 contains only the 225 largest blue chip companies and weights them according to their price.

Japan's economy is flourishing again

Japan's latest economic data looks promising. The economy has grown far more strongly than previously expected. In the second quarter, gross domestic product grew by 1.5% compared to the previous quarter, significantly exceeding expectations, which had been around 0.8%. Overall, economic growth thus increased by around 6% year-on-year. The driving factor behind this development was domestic consumption in particular. This developed strongly as a result of the reopening with the lifting of coronavirus restrictions. This also compensated for declining effects due to lower exports, which had recently been lower due to the global drop in demand for goods.

Last year, 2022, Japan's nominal GDP also reached a record level of over USD 4.2 trillion. However, Japan cannot escape the developments in the global economy. A slowdown in growth in the US and China could also have an impact on Japan's growth prospects. However, the recovery effects in Japan are even stronger in direct comparison to other countries and are continuing. Particularly in the areas of digitalization, automation and renewable energies, Japan is still at a relatively early stage by international standards and could offer corresponding investment opportunities in the future.

Monetary policy normalization and slight inflation provide a boost

In 2016, the Bank of Japan (BoJ) introduced the instrument of yield curve control, whereby government bonds are purchased in order to keep 10-year yields in a narrow band close to zero. The aim of the BoJ was to keep inflation permanently below the 2% mark.

Since then, the Japanese central bank has increasingly abandoned the monetary policy aegis of fixed upper limits for yields. Following the BoJ's decision, the yield on 10-year Japanese government bonds climbed to a nine-year high of 0.575%. While yields on the 10-year bond were initially only allowed to move 25 basis points around the 0 percent target, this has now risen to 50 basis points. According to estimates by some market participants, this limit is likely to be increased further over the next few years and may eventually be removed altogether. This market-influencing policy has often been criticized in the wider economic community because it distorts the yield curve and systematically removes liquidity from the market.

The BoJ's decision to adjust the target range for long-term interest rates could have far-reaching consequences for the international bond markets. Large amounts of Japanese capital have flowed into foreign markets since the turn of the millennium due to higher interest rates. It is estimated that around a third of all investment grade US bonds are in foreign hands. Up to 40 percent of this could be slumbering in Japanese portfolios alone. Accordingly, a repatriation of these funds could also have a significant impact on interest rates abroad.

In his most recent communication at the end of July 2023, the head of the central bank, Kazuo Ueda, attempted to put the scope of monetary policy normalization in Japan into perspective. According to him, yield curve control will merely be pursued more sustainably and not completely abolished, as some market participants already expect. In this respect, the yield curve will once again be increasingly left to natural market forces.

Inflation and currency trends

The increased inflationary momentum in Japan is one of the reasons for the gradual tightening of monetary policy. This is because expected inflation remains high, particularly on the corporate side. The central bankers have revised their inflation forecast for the current financial year (ending in March 2024) upwards by 0.7 percentage points to 2.5%. Most recently, the inflation rate was 3.3%, which is still at a tolerable level in an international comparison with the USA or Europe.

In addition, the change in interest rate policy has also had consequences for the Japanese currency (the yen), which has depreciated sharply and made the country's imports more expensive. Conversely, however, export-oriented Japanese companies are also benefiting from the weaker yen. In his speech, Kazuo Ueda also mentioned the weakness of the yen as one of the reasons for the higher interest rate tolerance

Corporate reporting season in Japan surprised positively

The Japanese fiscal year 2023 did not begin until April 2023 according to Japanese time calculations and the results of the reporting season have been surprisingly positive so far. The companies in the TOPIX® Index, which are among the largest and highest-turnover Japanese companies in the TSE First segment of the Tokyo Stock Exchange, exceeded analysts' expectations by an average of 30% in mid-July. Things went particularly well for those companies whose business is mainly focused on the domestic market. This is partly due to the current weakness of the yen and partly to the fact that some companies are more dependent than average on China and are currently facing some home-grown challenges of their own.

The Japanese economy is attracting foreign investors

The strong economy, low inflation combined with promising growth prospects and the reformed regulatory capital market rules by the central banks are making Japan attractive to investors again. After more than ten years, the inflow of foreign capital into the country is once again increasing significantly.

In addition, Japanese companies have a high positive cash flow and sufficient liquidity. Correspondingly attractive dividend yields and share buybacks also demonstrate the capital and growth strength of the companies. This has already been recognized by top international investors such as the Oracle of Omaha, Warren Buffett. Buffett recently increased his stake in five Japanese trading companies to 8.5 percent via his subsidiary National Indemnity Company. These include Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo. However, instead of investing in individual companies like Buffett or buying the broad Japanese benchmark index, it could be worthwhile to increase the weighting of individual companies or sectors.

The "Vontobel Japan Equity Strategy Index" could be an interesting alternative for investors who wish to focus on a selection of companies with a higher weighting of individual companies and sectors compared to the NIKKEI 225 and who could benefit in particular from the changed macroeconomic environment in Japan. The product could also be suitable for investors who do not wish to take a closer look at Japanese equities but still want to build up sector exposure.

Index concept Vontobel Japan Equity Strategy Index

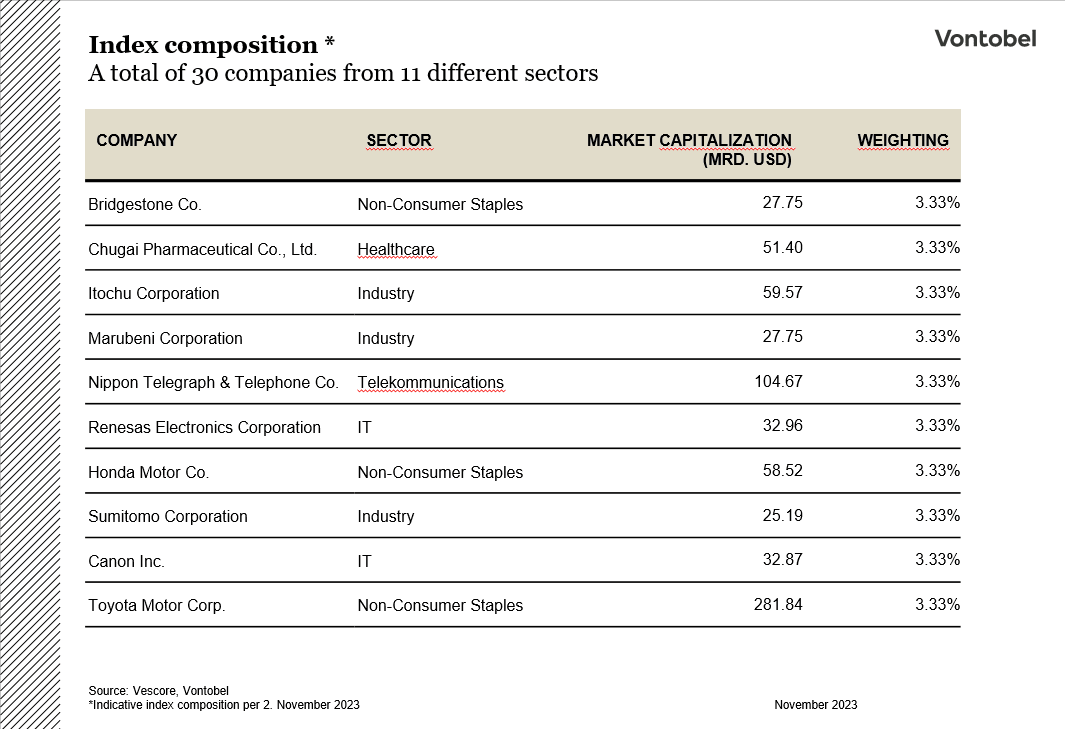

The selection of companies included in the index is determined by the index sponsor and is based on a factor-based model. Shares of medium-sized and large Japanese companies with attractive factor characteristics are selected. As part of the selection process, a composite multi-factor score based on the latest academic research is calculated for the companies based on the factors of valuation, quality, momentum and size. At the end of the selection process, the stocks of 30 companies with the highest multi-factor score are selected. This selection of companies is then equally weighted in the index. All companies taken into consideration must fulfill predefined liquidity criteria, taking into account the trading volume. The index composition is adjusted regularly (rebalancing) at least once a quarter.

At the end of this selection process, the Vontobel Japan Equity Strategy Index thus brings together those Japanese companies that could benefit from the changed economic and monetary policy environment in Japan against the backdrop of an attractive valuation. In this way, growth opportunities can be exploited in a targeted manner. It is not yet clear whether the current upturn in the Japanese stock market will continue. The following is an overview of ten exemplary companies from the index composition. The five trading companies favored by value investing legend Warren Buffett are also included in the index.

The changing economy could give Japanese equities a boost

Japan's long dormant phase seems to be over - the country is increasingly coming back into the focus of foreign investors. The promising economic conditions and the solidly capitalized corporate landscape also appear to offer potential in the medium to long term. Instead of spending a great deal of time searching for individual companies or investing in the broad market index, it can be worthwhile to give a higher weighting to individual companies or sectors. The Vontobel Japan Equity Strategy Index enables participation in the performance of 30 selected Japanese companies that appear attractive in terms of a multi-factor model (valuation, quality, momentum and size).

Risks

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

Product costs:

Product and possible financing costs reduce the value of the products.