Geopolitics and the gold price

During Friday, October 13, the price of gold in US dollar terms rose almost 3.5 percent due to escalating geopolitical unrest in Israel and a potentially dovish Federal Reserve following September's inflation numbers.

There is much that speaks for a higher gold price going forward, but historically, a major rise as a result of a geopolitical event has often led to an equal or greater fall in the price of gold soon after.

"Buy gold for troubled times" is the yellow stone's eternal slogan. Gold should act as a hedge against everything. Weak currency? Buy gold and hide it in the mattress and give it to your grandchildren. High inflation? Own gold. Is it war? Gold.

Already owning gold and buying gold are two different things. Gold tends, as in the example we are seeing right now, to rise in price, but short-term, during geopolitical unrest which provides a good opportunity for those who already own gold to sell and then buy back at lower levels just days later. Let's take a look at some historical examples.

Related Products

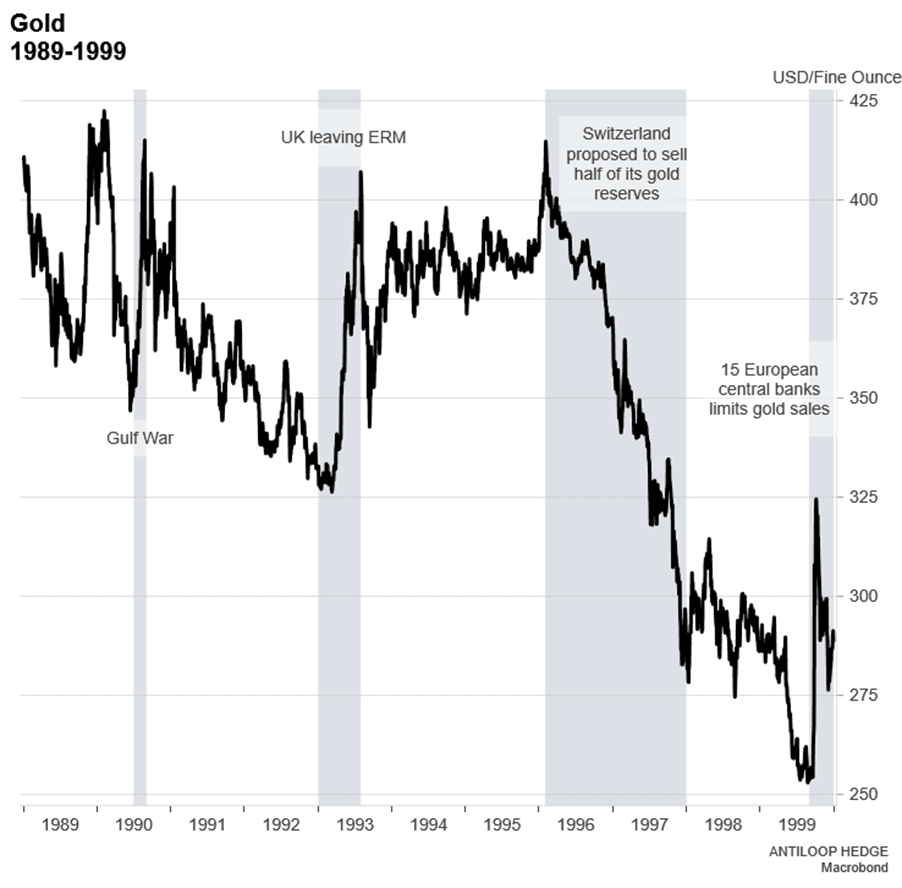

In the graph above, which shows the price of gold between the years 1989-1999, you can see, for example, how the Gulf War affected the price of gold in the short term, but that just as quickly as the price rose, it also fell shortly afterwards. The events that instead had a large and more long-term impact on the price were when Great Britain left the ERM in 1992 during the Sterling crisis. The fall of the British currency led to investors flocking to gold as a hedge against weak fiat currencies.

In 1996, instead, we saw the price of gold fall from record levels when Switzerland announced that it planned to sell half of its gold reserves. The price of gold then fell from over $400 and bottomed just above $250 before 15 European central banks got together and put a limit on how much gold they could sell. The price then reversed and rose to almost 325 USD in a short time.

Related Products

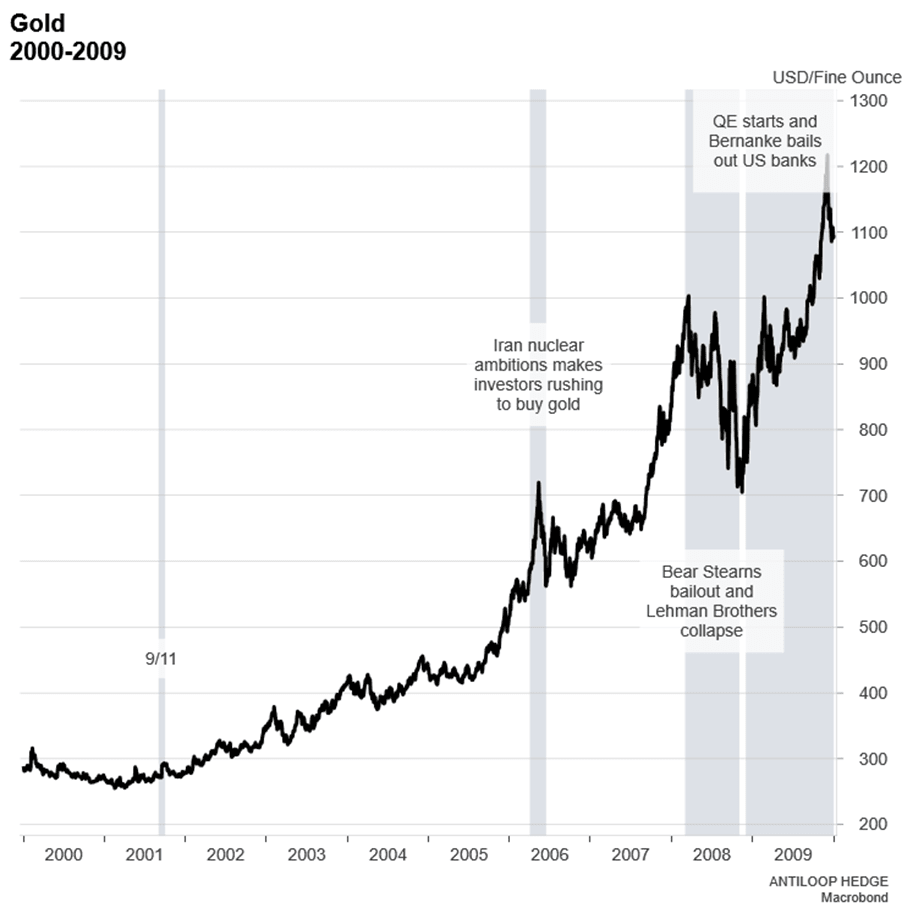

After 9/11, the price of gold also rose sharply initially but later fell back. Soon, however, a commodity boom began that would last until 2011 but was also reinforced by Bernanke's decision to bail out American banks and print money to stimulate the domestic economy out of the crisis. The gold price rose over 300 percent during the period.

Related Products

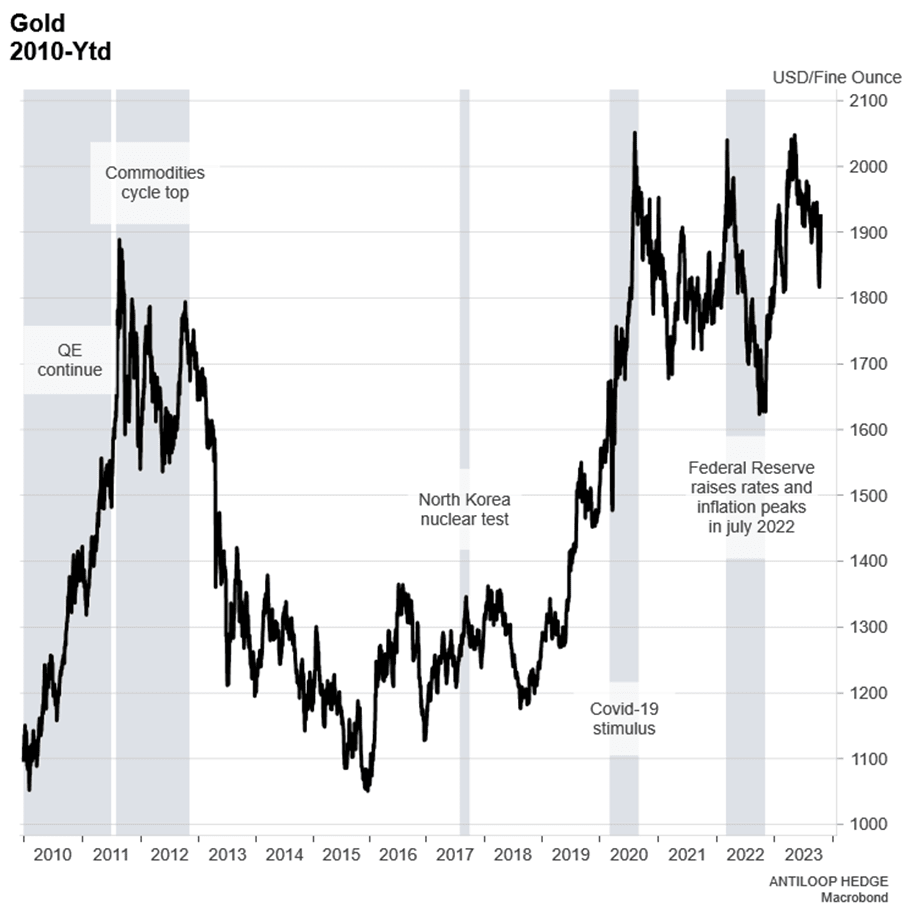

Between 2010 and today, we have been able to see the effect of Quantitative Easing (QE) on the price of gold, but also witnessed how the commodity cycle that started in the early 2000s peaked in 2011 when investors moved capital from commodities (and thus gold) to stocks. During September 2017, the price of gold rose to a yearly high when North Korea tested nuclear weapons, but the price fell equally during and after other geopolitical events and quickly returned again.

In 2018, the price of gold bottomed out at just under $1,200 and has since rallied to over $2,000 in three peaks in 2020 after Powell went from Hawk to Dove due to a pandemic and accelerated money printing that ultimately caused the Consumer Price Index (CPI) to go from “for low' to 'unexpectedly high' in the short term. The price of gold peaked along with inflation in July 2022 but has since risen again due to an expectation of future interest rate cuts and a deep recession as a consequence of the severe austerity the global economy has seen.

Long-term signals and short-term noise

Regardless of whether you invest in gold, other commodities or shares, it is important to learn to distinguish between short-term noise and long-term signals. Any event that affects the price of an asset in the short term but where the price soon returns to previous levels is noise and should only be used to rebalance a position you already have. Long-term signals, on the other hand, are what drive the price up or down in the long term.

The point of the examples above was to show that while major movements due to war or geopolitical unrest have often been short-term trend breakers, actions by central banks and concerns about the stability of the financial system have been what created long-term movements in real terms. In other words, gold is not a hedge against war, but merely a reflection of our trust in fiat currencies.

Maybe it 's different now

What potentially sets the conflict in Israel apart from previous geopolitical events and their effect on the price of gold is that what we are seeing now is potentially the start of a much larger global conflict. Biden and the US have said during the weekend of October 14-15 that they will support both Ukraine in the war with Russia, but that they will also continue to send financial support to Israel. A larger conflict and potential war where the US has greater involvement combined with an expected recession could mean further stimulus and thus a much higher price of gold.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.