Gruesome cyclicality and the price of time

Interest, and in particular the eighth wonder of the world interest on interest, has usually been considered something very bad, rather unholy, and in many cultures expressly forbidden

The time perspective is central to all investments. On that theme, I am currently reading the book The price of Time, which goes through what interest actually is and where it comes from, partly historically, partly economically. Interest, and in particular the eighth wonder of the world interest on interest, has usually been considered something very bad, rather unholy, and in many cultures expressly forbidden. Even where interest has been allowed, there have often been recurring, sometimes even regularly scheduled, debt amortization years.

The basic idea has been that interest on interest in particular is so burdensome for the borrower that there must be an upper limit to how long and how much one must pay on one's debt. The person who can afford to lend money is considered to know better than the person who borrows, and must therefore take responsibility for only lending to people who can actually afford to pay back on time without problems. If you still lend for consumption or to someone in need and poverty, society has chosen, after proven fact, to see it as a gift, and "freed" both borrowers and lenders from being burdened by a financial relationship that in practice has already ended.

In the US, you do not have to repay your mortgage if the value of the house is less than the loan amount. You can then safely lock the house, drop the keys in the letterbox and move to another state to start over. It follows the same historical principle as above, i.e. that you should not be able to become a serf because you happened to take out a larger loan than you could actually afford. It is the lender who must put an end to it. The bank should know better than to lend to those who really need the money and cannot get it in any other way.

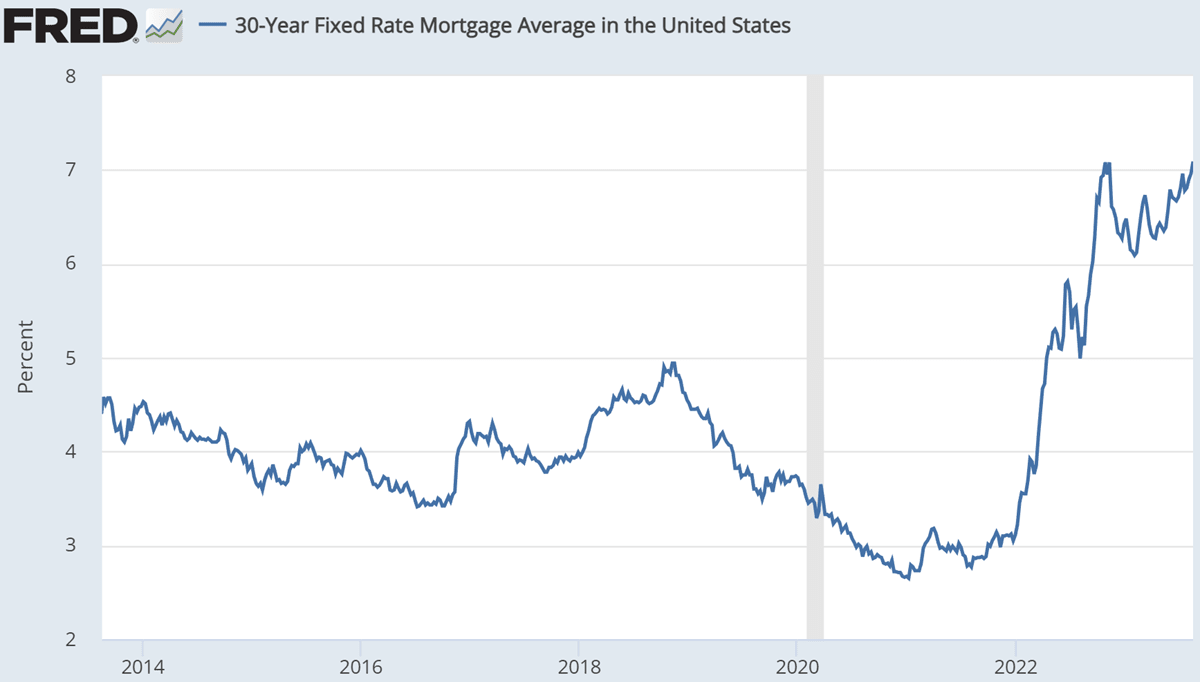

30-year mortgage rate in the US

The US mortgage market has more differences compared to e.g. Sweden. In the US, it is normal to borrow with 30-year interest. Right now, this mortgage interest rate in the US is 7.1% per year. The rise happened very quickly in 2022, so most have fixed their interest rate at only half that level, i.e. around the 3.5% that applied in the last ten years. When you sell your house and buy a new one, the loan and thus the interest rate are reset. Right now, this means double the interest cost for the new house. Because of this, extremely few have moved this year. You simply can't afford it unless it's the only way to get a new or much better paying job. A couple of years ago, just under 6% of all housing transactions were newly built houses. Now it is 31%, precisely because so few can afford to refinance their loans at double the interest rate.

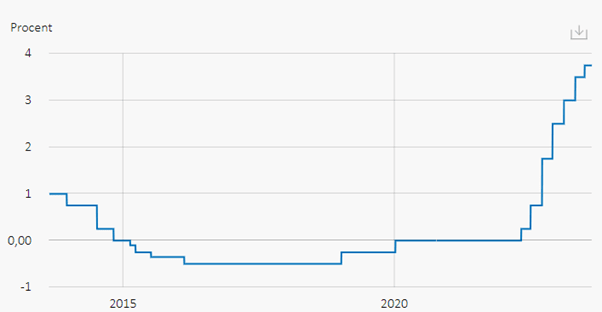

Factors like these delay the slowing effects of interest rate increases on the economy. What's worse is that it makes the economy less efficient when people who want or should move can't afford to do so. In Sweden, where the average bond period is approximately one year, it is faster, but even here there is at least one year left before the maximum negative effect of higher interest costs and weak demand due to interest costs is felt by households and companies. We are still raising the interest rate and a year ago we had barely started. The policy rate was 0.75% in August 2022, compared to today's level of 3.75%. The increase of a full three percentage points since then does not begin to be seriously felt until autumn 2024.

It's easy to forget that things actually take time. But just because we know about the rate hike doesn't mean it will affect anyone's consumption plans immediately. The costs have to rise for real first, and the money in the account has to run out before canceling the trip, buying shoes or changing grocery stores. We are so used to being able to message us and get a response in real time. We get news on everything from what a friend's friend has on their plate to the parliamentary situation in Niger the second it happens. Incidentally, there is a coup d'état in Niger in August, which very understandably has caused investors in GoviEx to sell their shares. In practice, the coup will likely mean nothing to the value of GoviEx, except for a little extra delay regarding the loan financing of the company's uranium mine in Niger. But you never know, the situation can of course worsen and drag on over time, even if coup d'etats in the area have historically not affected the mining companies significantly.

The Riksbank's policy rate

Mining companies are the archetype of cyclical industries. This is precisely because nothing happens at lightning speed in the extremely down-to-earth business of finding minerals, buying the land, ensuring the quality of the deposit, obtaining permits, arranging financing, buying machinery and other equipment, extracting and beneficiating the minerals and finally selling them at market price . To have the courage and strength to go through the process above, which is often measured in decades, one must be very sure that the price of gold, uranium, graphite, rare earth metals, copper, nickel, cobalt, or whatever one aims to extract in 10-20 -30 years will be high enough to justify all the costs and risks over 10-15 years associated with establishing the mine.

US 10-year Treasury yield

Related Products

The longer the lags and the greater the capital investment, the more cyclical the business. Mines are among the worst with huge investments years before any revenue. In addition, there is great uncertainty about the future price of the products, because you are forced to accept the prevailing market price. Copper is copper and gold is simply gold, even if you can try to differentiate your metals with e.g. an ESG certification.

When money is plentiful but metals are scarce, many mining projects are started. These are ready at about the same time, which leads to oversupply and low prices. If the mines are really unlucky, then there is both an abundance of metals and a shortage of money, i.e. higher interest rates, which causes double problems when the loans to build the mine have to be paid. This means that no one wants to start mines then, which later leads to mineral shortages and high metal prices. The cycle continues even though everyone knows about it, because when it looks attractive to start a mine, the margins look so huge that it is almost unthinkable that you should be able to lose on the project. Then, unfortunately, a bureaucratic long bench often follows. unexpected delays and costs, environmentalists, possibly involving geopolitical unrest, war, expropriation and coup d'état, not to mention natural disasters.

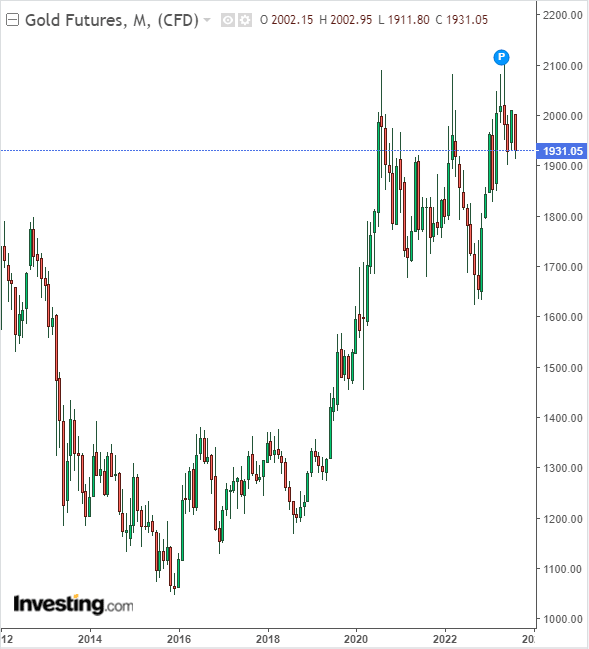

The life of a mine owner is rarely very fun. This is why all mines look extremely cheap on paper. All but the gold mines. Especially gold mines usually only look cheap if you count on the total amount of gold in the ground, or on future much higher gold prices, or that they are bought up. But calculated on rolling profit or cash flow, the gold mines are as expensive as hyped software companies or digital casinos. Incidentally, gold now looks ready for a phase shift with sharply rising prices, after ten years of sideways price development calculated in USD

Gold futures price, USD per ounce (31 grams)

There are, of course, no sure ways to make forecasts for the gold price, partly because of the long cycles in the mining industry. However, there are several indicators that are more or less historically correlated with the gold price, e.g. the money supply and the US gold reserve, as well as consumer price inflation and the key interest rate and bond yields. The time lags between the data series are long and varied, but there are nevertheless some logical patterns in the data material. When the government tries to stimulate the economy with subsidies, reduced interest rates and bond purchases, the price of gold usually rises. Like 2020. In troubled times, the price of gold usually gets an extra push upwards. Like 2016 and 2018-2019. During 2021-2023 there was a hangover for gold after the doubling in price since the bottom in 2016. The rapid interest rate hikes held back the price of gold because suddenly there were safe investment options that also gave a decent return. But in the background, price increases on everything else pushed on at a rapid pace. It is the inflation that is expected to have a positive effect on the gold price in the future when the bond alternative becomes less attractive when interest rates fall again.

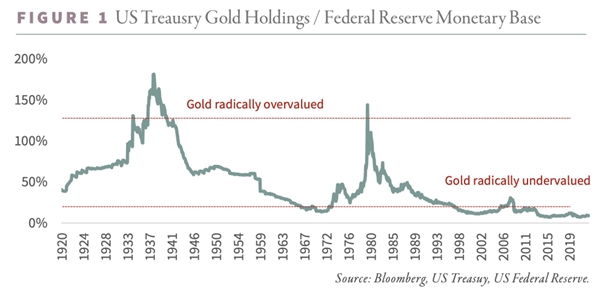

US gold reserves relative to the money supply

This is the importance of the right time perspective and the investor's best friend patience comes again. Money has been created, or at least bank reserves. The United States government is printing money in the form of huge fiscal deficits that are financed by the central bank and approved by politicians by effectively abolishing the debt ceiling for the foreseeable future. Fitch has therefore recently lowered the USA's credit rating, because Fitch sees that the USA's financing needs are not clearly resolved for the long term. There is thus much more money in circulation at the same time as the economy slowly manifests its underlying weakness as the effects of the pandemic measures subside. In that perspective, gold is "radically undervalued", but a trigger is needed that accelerates capital flows and changes portfolio weight preferences from zero or some/a few percent gold to 5-10 percent or more, depending on the type of investor.

That trigger is when the Fed openly admits that the economy is so weak that they have to cut interest rates. That is, when you make a pivot, a sudden reversal from austerity to stimulation. Especially if it happens at the same time as such an "inflationary echo" which historically has always been the norm after a strong inflationary impulse. The echo of a double or triple peak in measured price changes depends on how core inflation, wages and base effects co-vary with different lags seen over a couple of years.

Uranium is then a story in itself regarding the need for patience, both for the mining operators and for us ordinary consumers who would prefer to see reduced dependence on Russian oil, reduced Russian oil-financed military power, and above all secure access to sustainable and reliable base power. When sun, wind and water stand still due to the weather, only nuclear power can deliver green energy. It is also cheap if only the authorities let it be, for example by helping SMR technology (small. modular reactors) to break through.

The patience of uranium investors was severely tested after the Fukushima disaster in 2011, just when the industry appeared to be on the way to a breakthrough. Now it is bubbling again in earnest, not least in the form of tripled spot prices since the bottom, but also the amount of nuclear power construction with China at the forefront. Then it is extra difficult as an investor in GoviEx to have to see a coup d'état in one of their two key areas. Fortunately, the secured value of another of their deposits in a more stable area is more than double the market value of the entire company. In addition, as I said, things will work out in Niger as well. It is "just" a question of time perspective and patience. And we mining investors have plenty of that from the start. Therefore, it also applies to invest in several different mining assets in different geographies, from oil through safe COP or the slightly more speculative Africa Oil, to gold via Lundin Gold and EMX (gold and copper options) or Leading Edge Materials' prospective operations in graphite, rare earth metals , nickel and cobalt.

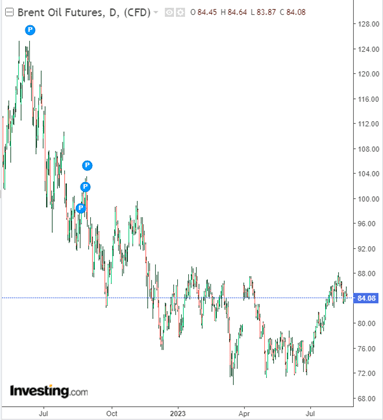

Oil price, Brent USD/barrel

Oil prices have made a bit of a comeback in July, but it's not quite convincing yet. If you have a long time perspective and can wait until 2024, it looks really positive. Right now, however, it is a little worrying that the US is emptying its oil reserve SPR and that the price is not higher than this despite voluntary production cuts in Opec+. It is probably the risk of recession that is haunting. 2024 looks set to be the Year of Patience for investors rather than the Year of the Green Tree Frog as the Chinese Zodiac calls the year. However, Africa Oil's shares have risen sharply despite everything.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.