Soft landing, right?

After the Federal Reserve's latest 25 bp hike, US interest rates are now at their highest level in 22 years.

In a year Powell has gone from predicting the "most anticipated recession ever" to saying on Wednesday that the Federal Reserve no longer believes that we are facing a recession in the US.The Federal Reserve believes they can keep the consumer price index down to low, sustainable levels without it having to have major consequences on the labor market.

Related Products

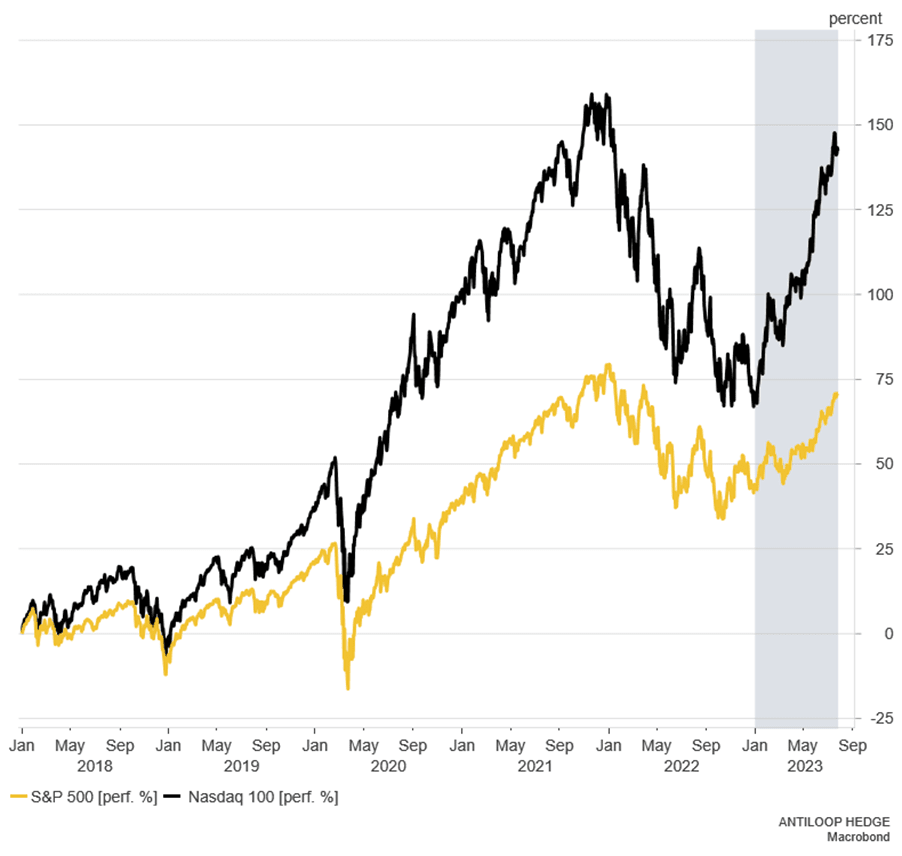

If you look at how the stock market has moved during the year, however, you cannot say that a recession has already been priced in. Since the turn of the year, the S&P 500 has risen over 20 percent and the Nasdaq over 44 percent. Despite the strong rise, there is a little bit left to the old All-Time-Highs: before the decline in 2022, the Nasdaq traded at levels above 16300 and the S&P 500 near 4800.

S&P500 and Nasdaq 100, in USD

Related Products

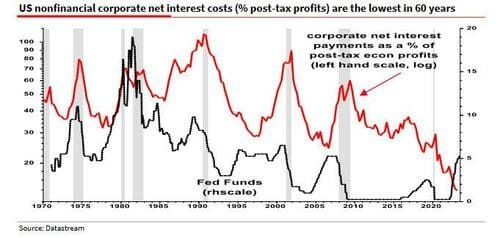

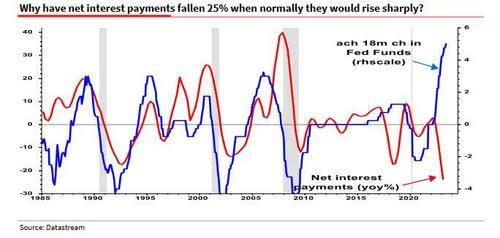

A cloud of worry that has hung over the market has been how companies with high debts will be able to parry the sharply rising interest rates. Several, the undersigned included, have been sure that rising interest rates would have negative effects on corporate profits, but instead the reverse has happened. Instead of the companies' interest costs rising as one might expect during a period of sharply rising interest rates, the companies' interest costs fell by 25 percent.

According to Albert Edwards at SocGen, what has happened is that companies have been able to take advantage of the yield curve to a large extent by locking in deposits at record low interest rates in 2020/2021 and at the same time being able to lend at higher interest rates now. Overall, it has led to companies becoming net recipients of interest costs and being able to increase profits as a result by 5 percent instead of profits falling by 10 percent or more as many expected.

Overall, Edwards believes that it is not only what is called "Greedflation" that has led to companies' profits rising (that is, companies raising prices until demand disappears and then lowering prices again) and thus a recession has not occurred without more people being able to benefit from rising interest rates via their balance sheets. In other words, high interest rates don't work the way they used to.

The question we have to ask ourselves now is; what happens to the demand for products and services if corporate profits continue to rise along with asset prices and how will this be reflected in consumer prices going forward if rising interest rates no longer have the same effect as before?