Little by little, and then all at once

Powell said a few weeks ago that the Federal Reserve saw no systemic risks from the rapidly rising interest rates. Then it narrowed.

It is not the first time a central bank governor has been wrong, of course. But that just a few days before a bank announces that they are forced to sell long government bonds at a loss because they simply start to realize that they will not have the coverage to pay out the funds that their customers put into regular deposit accounts which led to a bank run and then collapse is startling.

The market initially reacted with a sell-off. But instead of strengthening the dollar, the price of gold and bitcoin rose instead. Confidence in centralized finance and fiat appears to be about to be spent.

But how does a collapse of a financial system actually happen, and how can investors protect themselves against the inflation risk that we are now facing?

How did we end up here?

The banking crisis we are witnessing right now is not actually due to high interest rates. Rather, it is due to the fact that for many years the interest rate was so low that banks were forced to buy bonds with very long maturities in order to earn money on deposits.

When inflation took off, the Federal Reserve raised interest rates, and banks that had listened to Powell's forecasts that interest rates would not be raised anytime soon were left with deposits locked up in 10-year bonds that fell in value. At the same time, deposits at the bank fell as investors held onto their money more tightly. The willingness to take risks had basically disappeared.

However, the companies that used, for example, SVB as a bank had to continue paying their costs and the outflow from SVB eventually became so significant that they decided to divest government bonds and take a loss.

The collapse of SVB then sent shockwaves through the market and despite the fact that just a few days earlier Powell had said in front of Congress that there were no systemic risks, just such were discovered.

To avoid a complete bank run, the FDIC (US Federal Deposit Insurance Corporation) came to the rescue and all deposits were guaranteed while the owners and management of the bank were left naked.

What happens now?

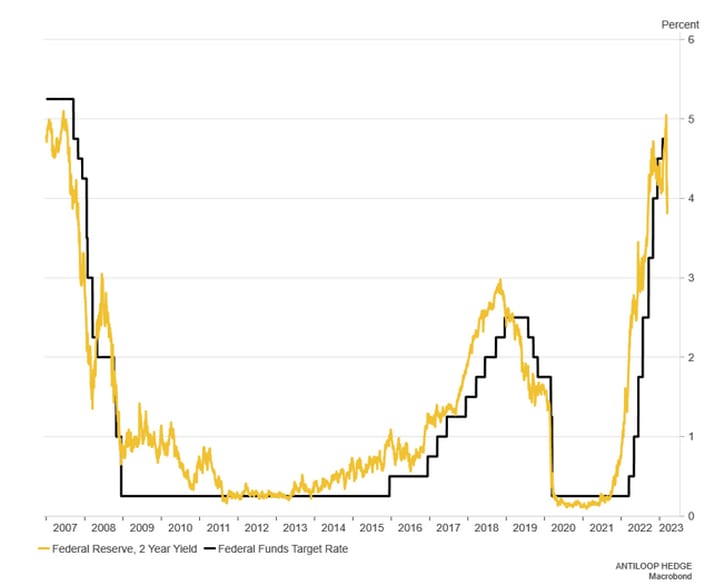

When it became clear that depositors were being protected - regardless of bank - the investor collective quickly realized that the market's brief spell of Quantitative Tightening was over. And, while the Federal Reserve has tried to maintain the belief that inflation must still be a priority with continued rate hikes, the US 2-year has fallen from over 5 percent on March 8 to 3.8 percent on March 17.

US Federal Reserve (Treasury Securities) 2-year yield vs. Federal Funds Target Rate

And it is precisely this that has led to the forgotten risk appetite of investors starting to find its way back again.

But, low interest rates and monetary policy stimulus don't just mean risk assets will go up. It also means that we are probably facing a new inflation peak in the future.

Inflation hedge

Although the price of gold has briefly risen to near peak levels against the US dollar, there could still be room on the upside. As the value of money devalues and confidence in central banks shrinks, more and more people - both private individuals, institutions and the central banks themselves - could buy more gold.

Related Products

Despite close to peak levels, gold is not very expensive, especially when compared to stocks, for example to the levels of the US S&P500 index in the past 40 years (chart above). Despite the recent upswing, there are many indications that the yellow stone is about to take revenge in the inflation hedge debate.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. This information is sponsored by Bank Vontobel Europe AG, which may be a counterparty to transactions involving the financial instruments discussed in this information. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.