Growth at any cost

Jeremy Powell's main focus is to extend the business cycle we have been in for the past decade. In an interview with Real Vision, Julian Brigden from MI2 talks about his view on macroeconomic developments right now and is similar to the current situation with 2015 and 2016 when we saw increased risk in Asia that caused central banks to push up monetary stimulus to continue driving growth.

Jeremy Powell's main focus is to extend the business cycle we have been in for the past decade. In an interview with Real Vision, Julian Brigden from MI2 talks about his view on macroeconomic developments right now and is similar to the current situation with 2015 and 2016 when we saw increased risk in Asia that caused central banks to push up monetary stimulus to continue driving growth.

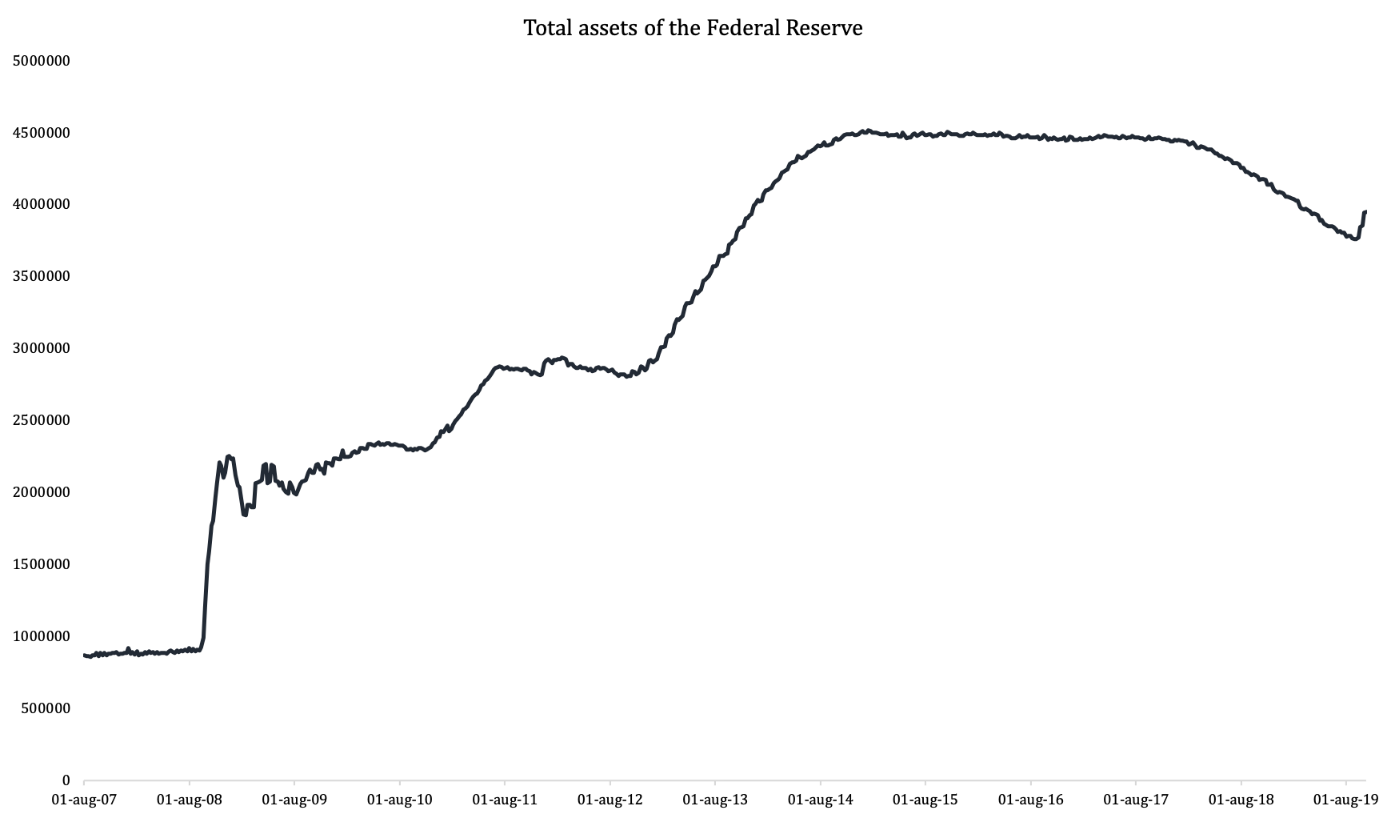

Since

the financial crisis, we have seen extreme monetary stimulus from the world's

central banks in an attempt not to end up on the slope again. Today,

Powell's main focus is to extend the cycle to keep up economic growth at all

costs, but to continue kicking the can in front of us will require even more of

the Fed, says Julian Brigden.

US economic

growth is currently dependent on keeping share prices up, interest rates low

and most importantly - weaker USD.

The

now more than 10-year boom has previously been challenged by macroeconomic

unrest, such as in 2015-2016, when Asia demonstrated weaker

growth, which caused central banks around the world to panic. They met in

Davos, and soon fiscal stimuli were switched over so as not to slow down

economic growth at all costs in the US as well. Now it's been another

three years and the toolbox is starting to echo empty, Powell himself has said

to then switch again to lower interest rates and smuggle QE programs (although

he was clear that what we see now is in fact something completely different).

However,

it is not risk-free to push the economy with strong stimulus without giving it

a chance to return to normal levels. Now we see more and more signs

of problems bubbling under the surface of the inflated asset bubble that

we are in. Companies such as Netflix and WeWork are two

examples of this, where the valuations in both cases are abnormally

high. House prices in the United States that have recovered after the

financial crisis, Julian Brigden says , are another good example

of highly valued assets.

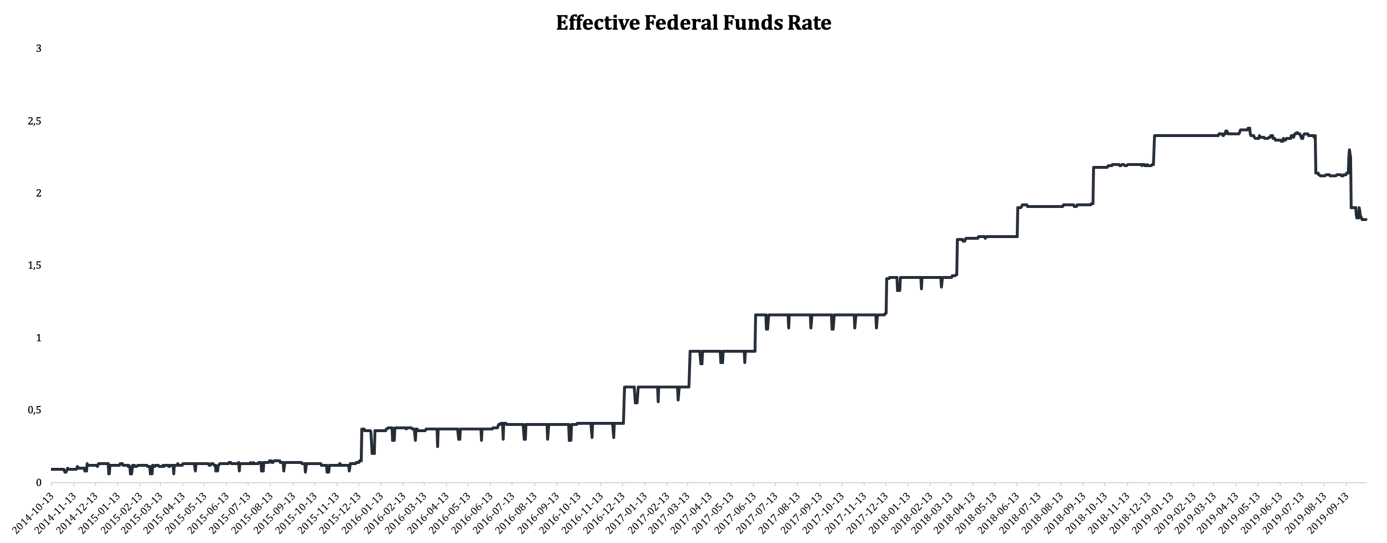

When

the Fed tried to normalize through monetary policy tightening in 2018, it

quickly had major consequences for the economy. The big problem here is

that financial markets have become leading the economy. In many cases, a

CEO of a listed company's job is about keeping the share price rising. This

means that if the Fed tightens monetary policy through QT and it has

consequences for the companies' share prices, it could lead to

the CEO over-looking costs, dismissing employees and not in the same

way daring to invest in their own operations because he or she must ensure so

that next quarter's results are better than expected to defend its valuation.

This

leads to the economy being extremely sensitive to downside

changes. Ben Bernanke has said that it is enough for

unemployment to rise by 0.3 percent to prevent the trend from

reversing. When so many people lose their jobs, he means that it creates a

great uncertainty that affects consumption and thus ultimately economic

growth. And even though the latest job numbers from the US came in at

perfectly okay levels, we can conclude that we seem to loose momentum.

What is the alternative for the Fed and investors in the future? Real monetary policy stimulus in the form of QE will be required. This could keep valuations at today's levels and even higher, which would mean that there is still some upside in the stock market, and above all, larger index overlapping companies.

@Anna Svahn

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.