The Chinese era is here

An earlier article discussed the life cycle of a fiat currency, using the US dollar as an example. Since the USD has functioned as a reserve currency since Bretton Woods in 1944, the currency is somewhat stronger than others as demand for the USD is generally higher. That is changing.

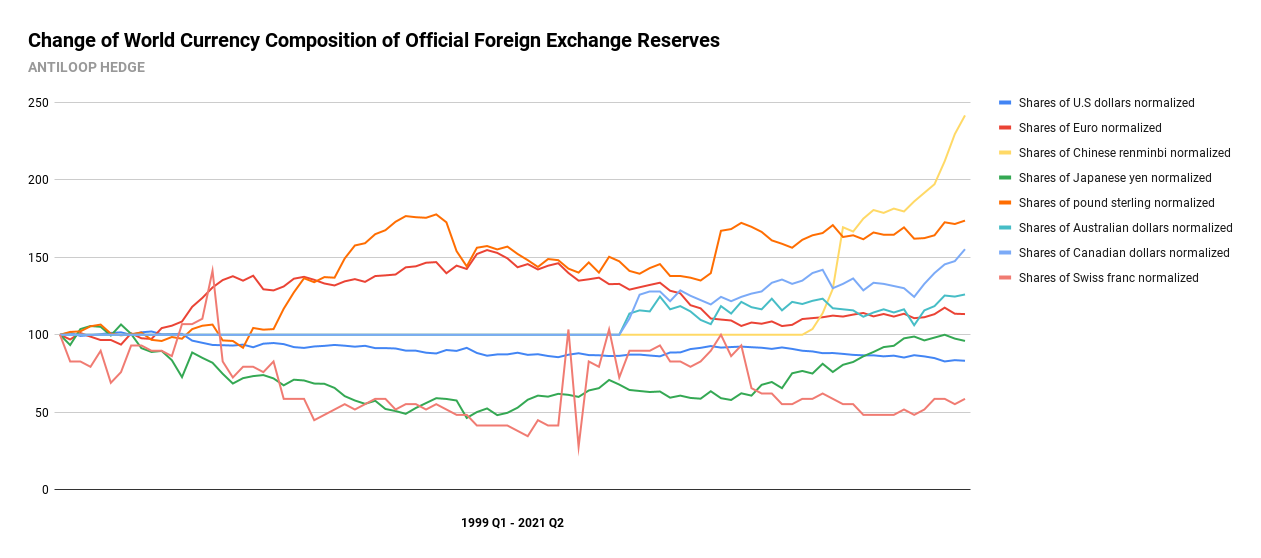

After a long period of strong stimuli, the US dollar has lost confidence among the countries that have historically filled their foreign exchange reserves with dollars. Instead of a single currency dominating global foreign exchange reserves, we are moving in a more and more diversified direction - and the currency that is growing the most seems to be the Chinese renminbi.

From not having been in global foreign exchange reserves at all, the renminbi has increased sharply since 2016. And although levels are still comparatively low, the yuan is expected to account for between 10-15 percent of global foreign exchange reserves in just 10 years.

China leaves nothing to chance. They have a hundred-year plan to become the most powerful economy in the world. That plan also includes allowing the yuan to take more and more place in global foreign exchange reserves.

During the pandemic, when the rest of the world's central banks barely breathed between squeezing more money to stimulate the economy, instead being more restrained, China has managed to keep its currency away from devaluation due to inflation, and now it is starting to show itself against the USD.

Gaining exposure to the Chinese market is difficult, and owning shares there involves higher political risk than in many other countries. If we also add to this the lack of transparency, which is a major problem when foreign investors buy Chinese companies, the overall risk level ends up high.

Exposing oneself to Chinese companies thus seems to be a tricky way of exposing oneself to the Chinese economy, and thus CNYUSD becomes a simpler exposure.

What drives the price

Although fiat currencies themselves feel like a thing of the past, we cannot really count them out yet. However, for those who still choose to have an exposure to fiat, it is important to simply choose the country which they believe will have the greatest influence in the future.

Before Bretton Woods in 1944, the global reserve currency was only an expression of the currency in which most transactions took place. Since most currencies before the First World War were still backed by gold, it can be said that gold itself should be considered our historical reserve currency - which was also the reason why it was ultimately the US dollar that took over the mission after 1944.

After World War I, many of the countries of the world were indebted to the United States, and at that time the United States owned more than half of all gold. This in turn led to the agreement that the US dollar would be our new reserve currency, rather than letting the gold become so immediately.

Since then, however, much has happened. In 1971, the United States left the gold standard, and instead of global currency reserves being indirectly backed by gold, they were backed by another fiat currency.

Since then, central banks themselves have chosen to buy gold, but in the last two decades have also chosen to diversify their foreign exchange reserves, from almost exclusively USD to a larger basket of different currencies.

What drives the price of the renminbi is thus the same as what has driven the price of the USD historically - confidence. China has de facto squeezed less money during the pandemic to avoid devaluation of the yuan, while more countries have also chosen to go from having no yuan in their reserves at all, to suddenly increasing that share sharply - quarter after quarter.

Strategic Certificates

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.