Falling supply and growing demand

Much of what is written about markets is about whether some asset is considered "cheap" or "expensive", and the writer builds a case for whether prices should go up or down. We hear about low and high Price/Earnings (P/E), rise or fall in cost of capital and various scenarios for future growth. There is undoubtedly a lot of intelligence, reason and experience behind this, and occasionally they hit the spot.

That is the story of "The Magnificent Seven"

However, if you have been a trader or investor for a while, you will have seen countless examples of apparently cheap stocks remaining cheap forever. Likewise you see extremely expensive shares become more and more expensive, and then perhaps change their trend a few months later. This maybe happens at the same time that the underlying development in the company is actually getting better and not worse. It is not uncommon to see the most well-informed analysts in an industry predict that the price trend will go in one direction, only to observe that the exact opposite happens.

Without attacking either theory or practice for such analyses, one can choose to focus on other angles, which can provide new insights into the market. Let’s start by noting the following:

1. All securities that exist must be owned by someone.

2. Some securities have a fixed/limited supply side, others have a flexible or almost infinite supply.

3. It is the daily balance between supply and demand that determines the prices we see traded.

What does this mean?

This has some interesting implications. If you buy a share, someone else has to sell it. If no one wants to sell the share at the price you want to buy at, you must increase your bid, and continue with this until you have filled up the volume you want to buy. A company can issue new shares in a secondary issue, or new shares can come via exercise of options to employees. This increases the supply. On the other hand, the company can choose to buy back and cancel its own shares. This typically happens at different phases in a company's life cycle. The number of shares is most often increased in an unprofitable growth phase where the company needs a lot of new capital to finance growth. Shares are bought back and deleted as an alternative or in addition to dividends when the company is mature and generating a lot of surplus capital.

But what happens to the pricing of a company if it has a falling supply (number) of shares, and at the same time a rising demand from buyers who need to get hold of shares regardless of pricing? Well, the logical thing to assume is that the price of the share compared to its income will go up and that the shares will become "expensive". But if it becomes too expensive, surely people will stop buying it? Well, it's not that simple. Welcome to The Magnificent Seven of 2023.

Related Products

The shares with the highest market weight in the USA have had several nicknames in recent years. For a time they were known as FAANG, but after Facebook changed its name to META and NVDA has grown into one of the largest, the 7 largest are now referred to as "The Magnificent Seven". These shares have gained such a high market value that it is starting to become a challenge for market-weighted indices such as the NASDAQ 100 and S&P 500. Last summer, I wrote that the NASDAQ 100 index took action to carry out a so-called "Special rebalancing", and this week did they did it again for the second half of the year. This is done simply because several of the shares have such a high market weight that they are bumping into the index's weighting limits. It can be mentioned that these limits are already above the limits for what normal mutual funds are allowed to have in individual companies according to the Norwegian Securities Act.

The fact that the companies that create the most financial value also achieve the greatest weighting is an in-built advantage of market-weighted indices. But it can also lead to some interesting effects, which is my point in this article. What happens if these successful companies start using their cash flow to buy back their own shares so that the supply is reduced? And this is happening at the same time that more and more people are investing in index funds that mechanically buy the shares according to the weighting they have in the index. Well, then one would expect them to eventually be priced unusually high.

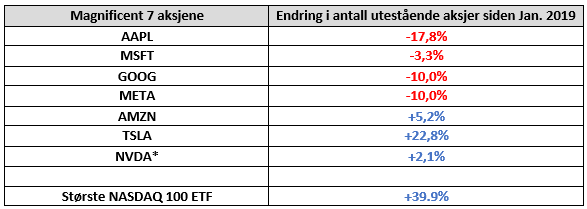

To illustrate this, I have looked at data for the development in the number of outstanding shares in The Magnificent 7 from the beginning of 2019 until the end of 3Q 2023.

Related Products

As we can see, four of the largest companies have had a significant reduction in the number of outstanding shares over the past 4 years. For NVDA, they have first had an increase, but then a decrease after March 2022. Amazon has had a small increase, while for TSLA, the number of shares has increased significantly. This is both because they made a secondary issue in 2020, but also as a result of an extensive option program having increased the number of shares.

At the bottom of the table, I have entered figures for the number of shares in the largest of the pure index ETFs that follow the NASDAQ 100 index. It is emphasized that this is only one of many such ETFs, and that there are also a number of traditional index funds that also follow the same weighting. ETFs are exchange-traded funds, so the number of shares is adapted to the flow of capital in and out. As we can see, the one I use as an example has increased its share count by almost 40% in the same period as several of the largest stocks in the index have reduced their share count. And there are many such funds competing for shares.

So we have companies that reduce their own number of outstanding shares at the same time as the demand for these shares increases from buyers who don't care about price. The index funds must hold these shares anyway.

Then they become expensive.

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the trading products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms. The base prospectus and final terms constitute the solely binding sales documents for the securities and are available under the product links. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.