Stable markets await ECB rate cuts

The Volatility Index (VIX) is currently trading around 15, compared with a peak of 38.57 in August, when higher Japanese interest rates, among other factors, contributed to a short-lived market shock. This is even though there are several uncertainties that could push the VIX higher again, such as the ongoing wars in Ukraine and the Middle East, and the fact that President-elect Trump will soon try to implement his trade proposals. Weak Purchasing Managers’ Index (PMI) data at the end of last week increases the likelihood of higher European Central Bank (ECB) rate cuts on the 12th of December.

Case of the week: Is VIX-mas coming early?

The CBOE Volatility Index (VIX) has been on a downward trend since the US elections. Far from the volatility spike seen in August, when it peaked at 38.57, the index is now trading around 15 at the time of writing. The 'fear gauge', as it is often called, has been calmed by some factors. However, we believe there is potential for a return to elevated levels in the short term.

Looking at the seasonal pattern of the index, November is almost always a downer. In fact, since 2010, the month has only posted a net gain four times out of the last fourteen years. November 2024 is not over yet, but with the index down 35.1% so far in November and only a few trading days to go, it is unlikely that the month will end on a positive note.

Looking at open interest and implied volatility, it appears that the market is not betting on a sharp rise in volatility. This is in line with the seasonal pattern, as December is on average a month with less movement in the index. President-elect Donald Trump added to the calming sentiment by naming Scott Bessent as his choice for Treasury Secretary.

However, there are still many notional rolls of the dice before the end of the year that, depending on the outcome, could add to market uncertainty. Sources of uncertainty include the ongoing wars in Ukraine and the Middle East, Trump's appointments in the US, policy and inflation expectations, and political uncertainty in the European Union.

There is a risk of escalation in the ongoing wars mentioned in Ukraine and the Middle East, which would certainly correspond to an increase in market fear, and thus a rise in the VIX. With Ukraine starting to fire long-range missiles into Russia in response to Russia's deployment of North Korean troops, there is a risk of further escalation. President-elect Trump and his running mate, JD Vance, have long said that they would quickly end the war in Ukraine. What this means in practice remains to be seen, as the method by which Trump will resolve the crisis has not yet been communicated. What is clear, however, is that the expected counter-offensive in the Kursk region will have a major impact on the course of the war.

During his election campaign, Trump was synonymous with increased protectionism through tariffs. This in turn has been associated with a potential dent in the otherwise falling inflation curve. With the risk of higher-for-longer interest rates, traders will once again pay close attention to upcoming triggers such as US Core Personal Consumption Expenditures Price Index and initial jobless claims. December's holiday shopping activity will provide some insight into the state of inflation, as prices could be pushed up by resurgent demand.

Finally, there is political turmoil in the EU. The EU's largest economy, Germany, is in bad shape. Unemployment is rising, while inflation has stabilised somewhat around the 2% target. Gross Domestic Product (GDP) growth is flat, and the governing coalition has collapsed. Socialdemokratische Partei Deutschlands (SPD) Chancellor Olaf Scholz will be nominated as the party's candidate for the next election, despite massive criticism from both inside and outside the party. By 2023, Germany will be the fifth largest importer of US goods, while the US will be the largest importer of German goods. If Trump exceeds expectations on tariffs, or if turbulence hits the German political scene, a corresponding rise in uncertainty should follow, leading to a spike in the VIX.

Putting all this together, there are some key areas of uncertainty that could impact the level of market fear, corresponding to a spike in the VIX. November 2024 has so far been the second worst year for the VIX over the 2010-2024 period. It remains to be seen whether December will follow the traditional pattern of the VIX experiencing a "Santa Rally" followed by a sell-off before the New Year. It should be noted that the various areas of uncertainty described above are very different from each other. With the exception of Trump's policy on the war in Ukraine, the outcome of one roll of the dice is not dependent on the outcome of another. With this in mind, the opportunistic trader can ask whether it is reasonable for the VIX to trade below an index value of 15 with so many dice in the air, or whether a rally in the VIX is in the cards for the coming weeks.

CBOE VIX, Hi-Lo seasonal pattern for December 2010-2024 (Indexed)

Related Products

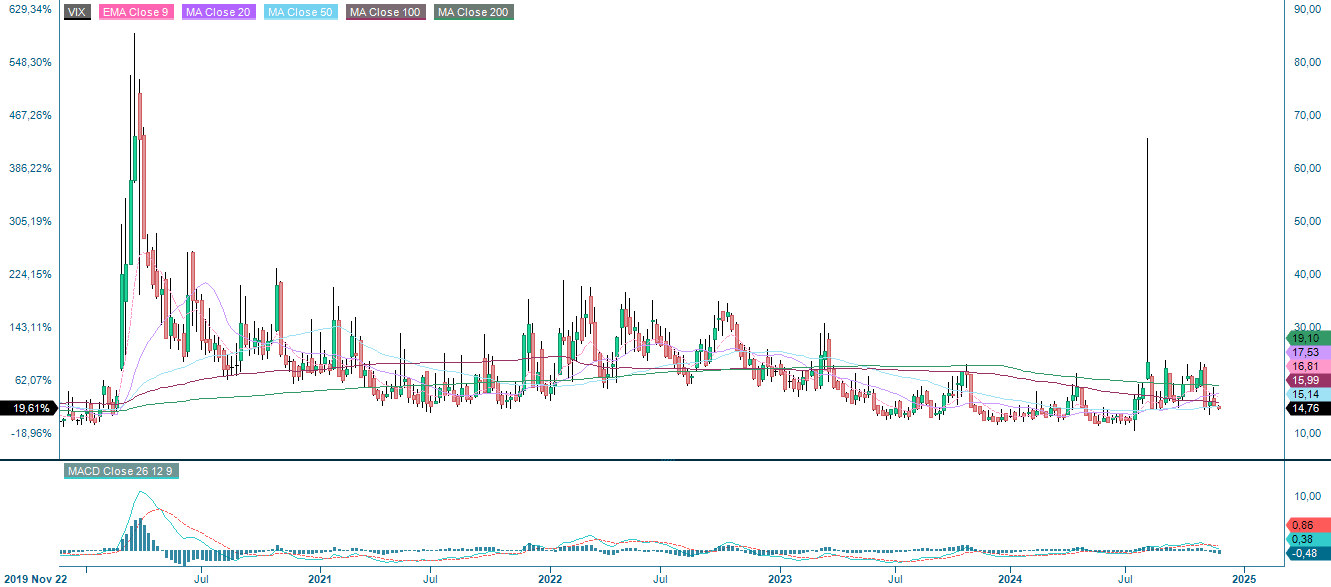

CBOE Volatility Index (VIX) Future (USD), one-year daily chart

CBOE Volatility Index (VIX) Future (USD), five-year weekly chart

Macro comments

The eurozone composite PMI fell to 48.1 in November from 50.0 in October. In the US, the economy is more dynamic and the composite PMI rose further to 55.3 from 54.1. The services sector is driving the US economy.

The weak PMI figure increases the probability of further rate cuts by the ECB in the next six months. Currently, there is a 50/50 chance of either a 25 or 50 basis point cut at the next ECB meeting on December 12.

German 2-year government bond yield (in %), weekly five-year chart

We start Wednesday 27 November with China's October industrial earnings. Some hours later we will receive German (GfK) Consumer Confidence for December and French Household Confidence for November. From the U.S., we get Q3 GDP, Durable Goods Orders, Personal Consumption and Inflation (PCE), and Wholesale Inventories, all for October. We also have initial jobless claims, the Chicago PMI for November, the Pending Home Sales for October and oil inventories (Department of Energy) weekly statistics. Interim reports from BAE Systems, Elekta and Lundbergs are due on Wednesday, while Norsk Hydro is holding a capital markets day.

On Thursday, 28th November, Statistics Sweden will publish the October Trade Balance. We also get Spanish and German Consumer Price Index (CPI) and a eurozone barometer indicator for November.

Friday, the 29th of November, starts with Japan's Industrial Production for October. This will be followed by Statistics Sweden's Retail Sales for October and Q3 GDP. Germany will publish import prices and retail sales for October and unemployment for November. France and Italy contribute with November CPI and France also with Q3 GDP. From North America, only Canada's Q3 GDP is on the agenda. The US will have a half day of trading (closing at 19.00 CET) due to Black Friday.

Time to establish new levels above 6,000 as yields fall?

The S&P 500 has bounced nicely off support and is now testing resistance around 6,000. The question is whether there is enough energy left. Well, looking at the Relative Strength Index (RSI), there is still plenty of room before this indicator turns overbought. Meanwhile, a further drop in US yields could provide a boost to equities.

S&P 500 (in USD), one-year daily chart

S&P 500 (in USD), weekly five-year chart

The Nasdaq 100 is also at resistance while the RSI is still in neutral territory.

Nasdaq 100 (in USD), one-year daily chart

Nasdaq 100 (in USD), weekly five-year chart

The DAX is also trading at resistance formed by the upper border of a descending channel. Note that the MACD has given a buy signal and the previous high of 19,660 could be the next target.

DAX (in EUR), one-year daily chart

DAX (in EUR), weekly five-year chart

It is not news that the OMXS30 has been relatively weak. The OMXS30 has been consolidating around resistance at 2,490. On a break to the downside, 2,400 could be next. On the upside, 2,555 is the first level of resistance. Therefore, going long on the OMXS30 is not a favourable trade from a risk/reward perspective.

OMXS30 (in SEK), one-year daily chart

OMXS30 (in SEK), weekly five-year chart

The full name for abbreviations used in the previous text:

EMA 9: 9-day exponential moving average

Fibonacci: There are several Fibonacci lines used in technical analysis. Fibonacci numbers are a sequence in which each successive number is the sum of the two previous numbers.

MA20: 20-day moving average

MA50: 50-day moving average

MA100: 100-day moving average

MA200: 200-day moving average

MACD: Moving average convergence divergence

Risks

Credit risk of the issuer:

Investors in the products are exposed to the risk that the Issuer or the Guarantor may not be able to meet its obligations under the products. A total loss of the invested capital is possible. The products are not subject to any deposit protection.

Currency risk:

If the product currency differs from the currency of the underlying asset, the value of a product will also depend on the exchange rate between the respective currencies. As a result, the value of a product can fluctuate significantly.

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Market risk:

The value of the products can fall significantly below the purchase price due to changes in market factors, especially if the value of the underlying asset falls. The products are not capital-protected

Product costs:

Product and possible financing costs reduce the value of the products.

Risk with leverage products:

Due to the leverage effect, there is an increased risk of loss (risk of total loss) with leverage products, e.g. Bull & Bear Certificates, Warrants and Mini Futures.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.