Investors’ Outlook: Budding hope

March provided investors with plenty of economic data to sift through in order to assess the investment environment. In keeping with the gradual arrival of spring, China's economic figures revealed quiet progress that could give cause for hope.

Springing forth

While US Federal Reserve (Fed) and European Central Bank (ECB) policymakers assessed the economic environment and contemplated the timing of interest-rate cuts, the Swiss National Bank (SNB) forged ahead, becoming the first major central bank to ease monetary policy. The move should help rein in the strong Swiss franc. Meanwhile, the Bank of Japan, which was “the last dove standing”, delivered its first rate hike in 17 years, ending its negative-interest era while scrapping its controversial yield curve control policy in place since 2016.

Recent inflation data came in stronger than expected, though it’s not likely to be much of a problem this year. Fed Chair Jerome Powell seems to share that view, saying the underlying story hasn’t changed. The Fed still expects to cut interest rates three times by the end of 2024. Considering stubborn service price inflation, central banks may start to cut a bit later and less than originally thought—but more than what’s currently priced in.

The Fed also updated its growth outlook. It now expects the world’s biggest economy to grow 2.1 percent in 2024, well above its December forecast of 1.4 percent. Despite higher growth, markets are more convinced rate cuts are coming. The ECB is also expected to deliver its first cut in the summer months.

In China, the government’s 5 percent growth target and the 3 percent inflation goal seems to be quite ambitious. The former faces challenging base effects, while the latter seems even more difficult considering China is currently flirting with deflation rather than inflation. There may be fiscal stimulus in the months ahead.

Checking the Old Continent’s economic temperature

Economists like to use the label “sick man of Europe” when referring to an economically ailing European state. In 2022 and 2023, a whole armada of “men” seemed to be suffering: Germany, Europe’s largest economy and heavily export-driven, was weighed down by weak demand from abroad, the aftermath of the 2022 energy crisis after Russia’s invasion of Ukraine, challenges in the domestic real estate market, and repeated protests. France and Italy also struggled with subdued industrial demand and workers going on strike.

After two years of below-average growth, the region’s economy has recently appeared to have stabilized somewhat. There are several reasons for this. On the one hand, the worst effects of higher interest rates seem to be behind us. According to the ECB’s Bank Lending Survey, European banks have significantly relaxed their lending standards in the last few months (see chart 1). At the same time, banks are expecting higher demand for credit in the second half of the year.

Lower inflation is a further tailwind. European producer prices have been in negative territory for months and fell by a further 8.6 percent year-on-year in January. This was partly due to significantly lower energy prices. Consumer prices are also on the right track, rising “just” 2.6 percent in February. However, certain expenditure items, such as services, remain stubbornly high at just under 4 percent. Services are considered the most complicated component of inflation, as wage growth in labor-intensive production is passed on with a considerable time lag.

Stabilization in the absence of significant economic acceleration

While lower interest rates and decreased inflation should provide a boost to the economy, there is little support from the fiscal side. According to the International Monetary Fund (IMF), European heads of state, unlike their American counterparts, are exercising fiscal restraint, which can, for example, be observed in the fact that the fiscal impulse has been shrinking for two years. In its forecasts, the IMF doesn’t foresee this impulse turning positive in the coming years. Consumers are unlikely to provide a significant uplift in the near future. While private consumption in the US has repeatedly surprised on the upside

and proven to be extraordinarily resilient, the story looks very different across the pond, where private consumption collapsed with the energy crisis and has not recovered since.

Current monetary policy is too restrictive

Be that as it may, the ECB is in no hurry to cut interest rates, with ECB President Christine Lagarde repeatedly referring to continued robust wage growth (see chart 2). As a result, along with many of her colleagues, she wants to wait for wage data to be published in the second quarter. Lagarde’s comment that we will know “a little bit” in April and “a lot more” in June could point to an initial interest-rate cut in June.

This fixation on wages seems misplaced. Firstly, wages are one of the most lagging indicators. The recent strong rise in wages can be viewed as a kind of catch-up process for real incomes (i.e., incomes adjusted for inflation). That’s because wages typically only react to past inflation. Secondly, certain core inflation measures developed by the ECB itself have already returned to the 2 percent inflation target (see chart 3).

Thirdly, a look at real interest rates (ECB refinancing rate minus core inflation) also shows that it is time for interest rate cuts: although the ECB has not raised interest rates for months, real interest rates have continued to rise steadily due to lower inflation (see chart 4), thus dampening the much-anticipated economic recovery.

First stirrings of easing

The unexpected rate cut by the SNB has solidified expectations for a worldwide easing of monetary policy, beginning this summer. Consequently, traders are now putting greater odds on a rate cut from the ECB in June, followed by the Fed and then the Bank of England (BoE). This prospect provides the bond market with a boost in the wake of the most recent Fed meeting.

During its March meeting, the Fed kept the federal funds rate target range unchanged and continued to signal that three rate cuts of 25 basis points each are the most probable course of action for 2024, despite recently stronger inflation. The summary of economic projections released after the Federal Open Market Committee (FOMC) meeting aligned with expectations, underscoring the confidence of policymakers in tackling inflation and securing a soft landing.

Surprising, and potentially more dovish, was Chair Jerome Powell’s frequent mention of the possibility that a rapid weakening of the labor market could lead to a faster decrease in policy rates. He clarified that while this scenario is not the FOMC’s base case, it outlines a possible risk. This is particularly relevant considering the hiring rate is already below pre-pandemic levels, suggesting that an increase in layoffs could abruptly shift hiring to negative territory and cause unemployment rates to rise.

The FOMC is poised to start reducing rates in June if there continues to be headway in the inflation picture.

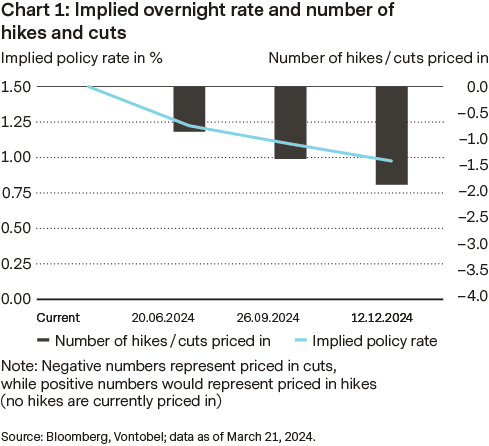

While incoming data remains strong, it is not strong enough to propel yields meaningfully higher from here, especially at a time when the Fed is biased to ease. The market is now fully aligned with the Fed in expecting three cuts this year (see chart 1). The longer the Fed keeps policy on hold, the greater the impact on the economy.

Navigating tight spreads: a case for caution in credit markets

Spreads have tightened significantly, coinciding with increased expectations for lower policy rates and a soft landing of the economy. They’ve only been tighter than current levels on a mere 6 percent of trading days in the last 25 years (see chart 2).

Equity markets in full bloom

Despite lingering concerns surrounding inflationary pressures, geopolitical tensions, and the uncertain trajectory of interest rates, stock markets have continued to move higher. Strong corporate earnings reports, especially in the US, and the perceived approach of central banks’ policy shifts fueled investor optimism.

Various indexes have flourished and reached milestones: the MSCI All Country World Index surpassed its all-time high of December 2021; the S&P 500 Index made history by crossing the 5,200-mark for the first time ever. And at the end of February, the Nikkei 225 Index finally surpassed its historic 1989 record (see chart 1).

The rally broadened further last month. Since mid-February, equity allocations by global institutional asset managers

have increased, according to Bank of America’s Global Fund Manager Survey. There was also a powerful style and sector rotation, with a greater focus on value and sectors such as financials, healthcare, consumer staples, energy, and real estate. Regionally, this resulted in higher allocations to European and emerging-markets equities, which outperformed US stocks. This was the case for Chinese and Swiss equities too.

What does this mean?

Retail investor sentiment became bullish in November, to the point of turning from cheerful to greedy, according to the American Association of Individual Investors’ Investor Sentiment Survey. This also means that most markets are facing an overbought situation, along with very high valuation multiples for some markets and sectors. This may have some wondering whether the rally is based on irrationality. Investors need to consider the drastic fundamental and structural change in equity markets that has occurred over the past decade. Taking the US technology sector as an example, the emergence of new structural megatrends resulted in stronger revenue growth, higher margin contribution, and free cash flow generation, which led to excess cash positions often returned to shareholders in terms of buybacks. This environment makes it hardly comparable with the dot-com bubble in 2000 (see chart 2).

The winds of geopolitics support oil

Oil prices got a geopolitical boost in March (see chart 1). The wind seems to be shifting increasingly in Russia’s favor, as Western support for Ukraine is waning. However, the latter has stepped up its attacks on Russian oil infrastructure and attacked numerous oil refineries.

The resulting reduction in Russian refinery capacity is exacerbating the situation for oil products. If Russia can’t process its crude oil, its stockpiles will rise. Russia has already announced that it will increase its oil exports. This is positive for oil products; but the higher supply is not necessarily great news for oil itself. In the absence of an escalation of the conflict, oil is likely to be supported at more than USD 80 per barrel.

“Dr. Copper” recovers (a little)

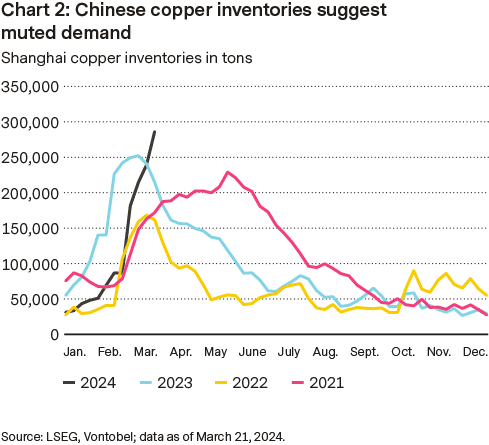

The recent rise in copper prices was primarily driven by a supply threat. After it was announced that loss-making Chinese copper smelters had jointly agreed to cut output, the red metal briefly approached the USD 9,000 threshold. However, no concrete details were provided, and the rally lost momentum again. There are still headwinds on the demand side. Investments in the Chinese real estate sector, which is important for copper, fell 9 percent in the January-February period. A look at the significant rise

in Chinese inventories also raises questions (see chart 2). Without significant stimulus or supply shocks, the upside potential is likely to be limited.

Gold shines

Gold reached an all-time high of more than USD 2,200 per ounce in March. While exchange-traded gold funds have long struggled with outflows—investors withdrew around USD 2.9 billion in February alone, according to the World Gold Council—the unabated strong demand from central banks has more than compensated for this. China’s central bank stands out in particular: it bought gold for the 16th month in a row in February and is now sitting on around 72 million ounces (+390,000 in February).

But China’s consumers have also made bold purchases despite high prices. One possible explanation could be the country’s economic context. While future central bank demand is difficult to predict (and data on this is published with a lag), gold is likely to benefit from the prospect of a weaker US dollar and lower US real interest rates. There should also be some support on the geopolitical front in the coming months, mainly from the war in Ukraine, the tensions in the Middle East, and the upcoming US presidential election.

The SNB rings in the rate-cut season

The Swiss central bank took the first step by reducing its key interest rate by 0.25 percent on March 21, setting the new policy rate at 1.5 percent from a previous 1.75 percent. This decision placed the SNB ahead of its global counterparts, which are expected to follow with similar rate cuts in the near future.

The move came as a surprise to many analysts, who had predicted that the central bank would keep its policy rate steady at 1.75 percent. SNB President Thomas Jordan noted that effective measures to tame inflation over the last two and a half years facilitated the step. Furthermore, the SNB lowered its inflation forecast to 1.4 percent for 2024, down from its December prediction of 1.9 percent. Historically, the SNB has not shied away from stunning the market with sudden moves, and this rate cut could be seen as a continuation of that trend. Noteworthy moments in its past include dropping the Swiss franc’s cap against the euro in 2015 and the unexpected 50 basis-point rise in borrowing costs in 2022. The SNB’s policy path for the remainder of the year suggests a bias towards further easing, with currently close to two further cuts priced in (see chart 1), bringing the policy rate to 1 percent by the end of the year.

Eyeing the US presidential election

The euro-dollar exchange rate is currently largely influenced by expected action from central banks. However, the upcoming presidential election in the US will increasingly play a significant role in market considerations, particularly with Donald Trump leading President Joe Biden in recent polls (see chart 2). Should Trump secure a victory in 2024, the economic stimulus from tax cuts and business-friendly policies seen in 2016 might not be replicated, given the current low tax rates and substantial budget deficits.

The combination of fiscal and monetary policy could result in more restrictive fiscal measures alongside looser monetary policy, potentially benefiting the euro-dollar exchange rate. On the other hand, a second term for Trump could potentially lead to a stronger US dollar due to safe-haven investments, aggressive foreign policies, and concerns about renewed trade tensions.

Authors

Frank Häusler, Chief Investment Strategist

Stefan Eppenberger, Head Multi Asset Strategy

Christopher Koslowski, Senior Fixed Income & FX Strategist

Mario Montagnani, Senior Investment Strategist

Michaela Huber, Cross-Asset Strategist

Risks

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.