Will we have a white Christmas?

It was a historically tight presidential race in Brazil, ending with the win of Luiz Inácio Lula da Silva, better known as Lula. The left-wing politician and former metal worker clinched the vote at the last minute, edging out Bolsonaro with 51 % of the vote. This coincides with sugar production supply possibly not meeting demand, as ethanol production wins favour. The win of Lula opens a potential shift in market sentiment for sugar prices by removing a price cap on biofuels.

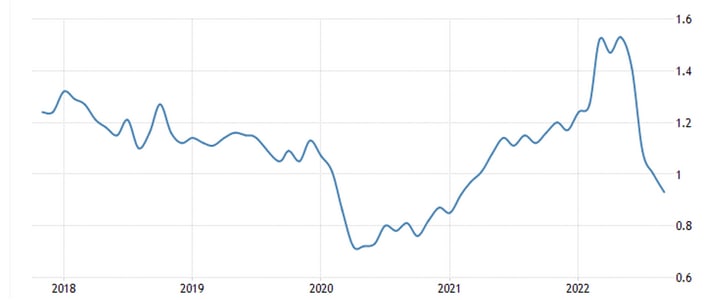

In the middle of the summer, then-incumbent Bolsonaro passed laws capping the price of fuel, trying to stem the rapid increase in prices since the start of 2022. With high inflation and rising fuel prices, the price cuts forced the state-owned company Petrobras to reduce their output prices to levels nearing 2020. That was a move that probably helped sate the increasingly displeased population. Inconsequential of the political aspect of the price cuts, they put a blanket over E25 and E100 prices, meaning, in turn, that more canes could be crushed and sold as white sugar.

Gasoline prices (USD/Litre), a monthly five-year chart, Sep-22 reference

Lula has previously promised to decouple fuel prices from the broader economic system; more precisely, he has stressed that domestic fuel prices must not depend on an international benchmark. Since the original removal of the gasoline price gap in 2016, following a five-year stint with regulated prices, ethanol prices have covaried closely with domestic gasoline prices. This was the case until 2022, however, when prices diverged, and ethanol dropped heavily after the previously mentioned price cuts. With expectations of the current price cap being removed at the beginning of next year, this should make the pendulum swing the other way, raising prices on biofuels such as ethanol. This is further supported by sugar approaching the back half of the season with, despite a 59 % increase in harvest yield during the first half of October, production being weaker this harvest season.

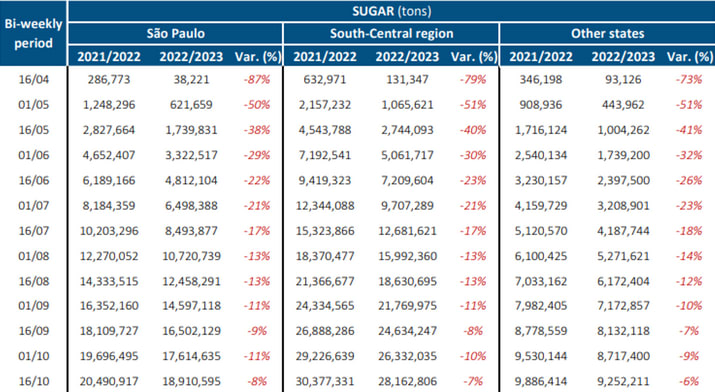

Bi-weekly accumulated sugar production (tons)

Sugar has been slumping in price during the year but might be in for a rebound. More precisely, if gasoline prices increase the demand for alternative fuels such as ethanol should increase. As this demand increases more sugar canes go to ethanol production rather than white sugar production. Assuming demand remains constant, supply should slip relative demand, and prices might rally for Christmas.

White Sugar Future Mar23 (USD/tonne), daily one-year price chart

White Sugar Future Mar23 (USD/tonne), a daily six-month price chart

White Sugar Futures(USD), five years

Risks

External author:

This information is in the sole responsibility of the guest author and does not necessarily represent the opinion of Bank Vontobel Europe AG or any other company of the Vontobel Group. The further development of the index or a company as well as its share price depends on a large number of company-, group- and sector-specific as well as economic factors. When forming his investment decision, each investor must take into account the risk of price losses. Please note that investing in these products will not generate ongoing income.

The products are not capital protected, in the worst case a total loss of the invested capital is possible. In the event of insolvency of the issuer and the guarantor, the investor bears the risk of a total loss of his investment. In any case, investors should note that past performance and / or analysts' opinions are no adequate indicator of future performance. The performance of the underlyings depends on a variety of economic, entrepreneurial and political factors that should be taken into account in the formation of a market expectation.

Disclaimer:

This information is neither an investment advice nor an investment or investment strategy recommendation, but advertisement. The complete information on the products (securities) mentioned herein, in particular the structure and risks associated with an investment, are described in the base prospectus, together with any supplements, as well as the final terms relating to the securities. The base prospectus and final terms constitute the solely binding sales documents for the products mentioned herein. It is recommended that potential investors read these documents before making any investment decision. The documents and the key information document are published on the website of the issuer, Vontobel Financial Products GmbH, Bockenheimer Landstrasse 24, 60323 Frankfurt am Main, Germany, on https://prospectus.vontobel.com and are available from the issuer free of charge. The approval of the prospectus should not be understood as an endorsement of the securities. The securities are products that are not simple and may be difficult to understand. This information includes or relates to figures of past performance. Past performance is not a reliable indicator of future performance. This information may only be distributed or published in countries where such distribution or publication is permitted by applicable law. As stated in the relevant base prospectus, the distribution of the securities mentioned in this information is subject to restrictions in certain jurisdictions. This advertisement may not be reproduced or redistributed without prior permission by Vontobel.

© Bank Vontobel Europe AG and / or affiliated companies. All rights reserved.